Federal Law 212 Federal Law of the Eurasian Union. Who makes contributions to the Pension Fund and when?

1. The object of taxation of insurance premiums for payers of insurance premiums specified in subparagraphs “a” and “b” of paragraph 1 of part 1 of this Federal Law are payments and other remunerations accrued by payers of insurance premiums in favor of individuals within the framework of labor relations and civil relations. legal agreements, the subject of which is the performance of work, the provision of services, under copyright contracts, in favor of the authors of works under agreements on the alienation of the exclusive right to works of science, literature, art, publishing license agreements, license agreements on granting the right to use works of science, literature, art, including remunerations accrued by organizations for managing rights on a collective basis in favor of authors of works under agreements concluded with users (with the exception of remunerations paid to persons specified in paragraph 2 of part 1 of this Federal Law). The object of taxation of insurance premiums for payers of insurance premiums specified in subparagraph "a" of paragraph 1 of part 1 of this Federal Law also includes payments and other remunerations accrued in favor of individuals subject to compulsory social insurance in accordance with federal laws on specific types of compulsory social insurance. insurance.

2. The object of taxation of insurance premiums for payers of insurance premiums specified in subparagraph "c" of paragraph 1 of part 1 of this Federal Law is recognized as payments and other remuneration under employment contracts and civil contracts, the subject of which is the performance of work, the provision of services paid by payers insurance premiums in favor of individuals (except for remunerations paid to persons specified in paragraph 2 of part 1 of this Federal Law).

3. Payments and other remunerations made within the framework of civil contracts, the subject of which is the transfer of ownership or other proprietary rights to property (property rights), and contracts related to the transfer of property for use (property rights) do not apply to the object of taxation of insurance premiums rights), with the exception of copyright contracts, contracts on the alienation of the exclusive right to works of science, literature, art, publishing license agreements, license agreements on granting the right to use works of science, literature, art.

4. Payments and other remunerations accrued in favor of individuals who are foreign citizens and stateless persons under employment contracts concluded with a Russian organization for work are not recognized as an object of taxation for payers of insurance premiums specified in paragraph 1 of part 1 of this Federal Law in its separate division located outside the territory of the Russian Federation, payments and other remuneration accrued in favor of individuals who are foreign citizens and stateless persons in connection with their activities outside the territory of the Russian Federation within the framework of concluded civil contracts , the subject of which is the performance of work, the provision of services.

5. Payments made to volunteers as part of the execution of civil contracts concluded in accordance with Article 7.1 of the Federal Law of August 11, 1995 N 135-FZ “On Charitable Activities and Charitable Organizations” to reimburse the expenses of volunteers are not subject to insurance premiums. , with the exception of food expenses in an amount exceeding the daily allowance provided for in paragraph 3 of Article 217 of the Tax Code of the Russian Federation.

6. Payments made to volunteers within the framework of civil contracts concluded in accordance with paragraph 4 of part 2 of the Federal Law of December 1, 2007 N 310-FZ “On the organization and holding of the XXII Olympic Winter Games and XI Paralympic Winter Games 2014 in the city of Sochi, the development of the city of Sochi as a mountain climatic resort and amendments to certain legislative acts of the Russian Federation", to reimburse the expenses of volunteers associated with the execution of these agreements, in the form of payment for the costs of processing and issuing visas, invitations and other similar documents, the cost of travel, accommodation, food, training, communication services, transport support, linguistic support, souvenirs containing the symbols of the XXII Olympic Winter Games and the XI Paralympic Winter Games of 2014 in the city of Sochi, as well as the amount of insurance premiums (insurance contributions ) under insurance contracts in favor of these persons, including the types of insurance established by the agreement concluded by the International Olympic Committee with the Russian Olympic Committee and the city of Sochi for the holding of the XXII Olympic Winter Games and XI Paralympic Winter Games in 2014 in the city of Sochi.

8. Payments made to foreign citizens and stateless persons under employment contracts or civil contracts concluded with FIFA (Federation Internationale de Football Association), FIFA subsidiaries, the Organizing Committee "Russia-2018" do not apply to the object of taxation of insurance premiums ", subsidiaries of the Organizing Committee "Russia-2018" and the subject of which are the performance of work, provision of services, as well as payments made to volunteers under civil contracts concluded with FIFA, subsidiaries of FIFA, the Organizing Committee "Russia-2018" and whose subject of activity is participation in events provided for by the Federal Law “On the preparation and holding in the Russian Federation of the 2018 FIFA World Cup, the 2017 FIFA Confederations Cup and amendments to certain legislative acts of the Russian Federation”, to reimburse the expenses of volunteers in connection with execution of the specified agreements in the form of payment of expenses for registration and issuance of visas, invitations and similar documents, payment of travel costs, accommodation, meals, sports equipment, training, communication services, transport support, linguistic support, souvenirs containing the symbols of the FIFA World Cup 2018, FIFA Confederations Cup 2017, held in the Russian Federation.

9. Payments and other remunerations made in favor of foreign citizens and stateless persons who are participants and members of the jury of the XV International Competition named after P.I. are not recognized as subject to insurance premiums. Tchaikovsky.

The provisions of Article 7 of Law No. 212-FZ are used in the following articles:- The basis for calculating insurance premiums for payers of insurance premiums making payments and other benefits to individuals

1. The base for calculating insurance premiums for payers of insurance premiums specified in subparagraphs “a” and “b” of paragraph 1 of part 1 of article 5 of this Federal Law is determined as the amount of payments and other remunerations provided for in part 1 of article 7 of this Federal Law, accrued payers of insurance premiums for the billing period in favor of individuals, with the exception of the amounts specified in Article 9 of this Federal Law.

Home » Federal Law on the Pension Fund, Social Insurance Fund, Compulsory Medical Insurance Fund » All about insurance premiums » Useful articles » Article 8 of the Federal Law 212-FZ

Attention! since 2017 A new Section XI Insurance Contributions has been introduced into the Tax Code of the Russian Federation.

See the full text of the Federal Law of July 24, 2009. No. 212-FZ

Article 8. Base for calculating insurance premiums for payers of insurance premiums making payments and other remuneration to individuals

1. The base for calculating insurance premiums for payers of insurance premiums specified in subparagraphs “a” and “b” of paragraph 1 of part 1 of article 5 of this Federal Law is determined as the amount of payments and other remunerations provided for in part 1 of article 7 of this Federal Law, accrued payers of insurance premiums for the billing period in favor of individuals, with the exception of the amounts specified in Article 9 of this Federal Law.

2. The base for calculating insurance premiums for payers of insurance premiums specified in subparagraph "c" of paragraph 1 of part 1 of article 5 of this Federal Law is determined as the amount of payments and other remunerations provided for in part 2 of article 7 of this Federal Law for the billing period in favor of individuals, with the exception of the amounts specified in Article 9 of this Federal Law.

3. Payers of insurance premiums specified in clause 1 of part 1 of Article 5 of this Federal Law determine the base for calculating insurance premiums separately in relation to each individual from the beginning of the billing period after each calendar month on an accrual basis.

For reference:

The base for calculating insurance premiums, taking into account its indexation, in relation to each individual is established in an amount not exceeding:

— from January 1, 2014 — 624,000 rubles(Resolution of the Government of the Russian Federation dated November 30, 2013 N 1101);

— from January 1, 2013 — 568,000 rubles(Resolution of the Government of the Russian Federation dated December 10, 2012 N 1276);

— from January 1, 2012 — 512,000 rubles(Resolution of the Government of the Russian Federation dated November 24, 2011 N 974);

— from January 1, 2011 — 463,000 rubles(Resolution of the Government of the Russian Federation dated November 27, 2010 N 933).

4. For payers of insurance premiums specified in paragraph 1 of part 1 of Article 5 of this Federal Law, the base for calculating insurance premiums in relation to each individual is established in an amount not exceeding 415,000 rubles on an accrual basis from the beginning of the billing period, unless otherwise provided herein Federal law. Insurance premiums are not collected from amounts of payments and other remuneration in favor of an individual that exceed the maximum base for the calculation of insurance premiums established for the corresponding financial year, determined on an accrual basis from the beginning of the billing period, unless otherwise provided by this Federal Law.

(as amended by Federal Laws dated December 3, 2011 N 379-FZ, dated December 28, 2013 N 421-FZ)

For reference:

Provisions of Part 5 This article does not apply when calculating insurance premiums at additional rates established by Articles 33.2 of the Federal Law of December 15, 2001 N 167-FZ and 58.3 of this document, in relation to payments in favor of insured persons engaged in work provided for in paragraphs 1 - 18 of part 1 of the article 27 of the Federal Law of December 17, 2001 N 173-FZ (Part 3 of Article 33.2 of the Federal Law of December 15, 2001 N 167-FZ, Part 3 of Article 58.3 of this document).

5. The maximum value of the base for calculating insurance premiums established by part 4 of this article is subject to annual (from January 1 of the corresponding year) indexation taking into account the growth of average wages in the Russian Federation, unless otherwise provided by this Federal Law. The size of the specified maximum base for calculating insurance premiums is determined and established by the Government of the Russian Federation. The size of the maximum base for calculating insurance premiums is rounded to the nearest thousand rubles. In this case, the amount of 500 rubles or more is rounded up to the full thousand rubles, and the amount less than 500 rubles is discarded.

(part 5 ed.

OKVED for the application of clause 8, part 1, article 58 No. 212-FZ of July 24, 2009

Federal laws dated October 16, 2010 N 272-FZ, dated December 28, 2013 N 421-FZ)

5.1. For payers of insurance premiums specified in paragraph 1 of part 1 of Article 5 of this Federal Law, for the period 2015 - 2021, the maximum value of the base for calculating insurance contributions for compulsory pension insurance paid to the Pension Fund of the Russian Federation is established annually by the Government of the Russian Federation, taking into account certain for the corresponding year the average salary in the Russian Federation, increased by twelve times, and the following increasing coefficients applied to it for the corresponding financial year:

|

Size of increasing factors |

The size of the specified maximum value of the base for calculating insurance premiums is rounded to the nearest thousand rubles in the manner established by part 5 of this article.

(Part 5.1 introduced by Federal Law dated December 28, 2013 N 421-FZ)

5.2. The maximum value of the base established by part 5.1 of this article for calculating insurance contributions for compulsory pension insurance paid to the Pension Fund of the Russian Federation, from 2022, is subject to annual indexation (from January 1 of the corresponding year) in the manner established by part 5 of this article.

(Part 5.2 introduced by Federal Law dated December 28, 2013 N 421-FZ)

6. When calculating the base for calculating insurance premiums, payments and other remuneration in kind in the form of goods (work, services) are taken into account as the cost of these goods (work, services) on the day of their payment, calculated on the basis of their prices specified by the parties to the contract, and with state regulation of prices (tariffs) for these goods (works, services) based on state regulated retail prices. In this case, the cost of goods (works, services) includes the corresponding amount of value added tax, and for excisable goods, the corresponding amount of excise taxes.

7. The amount of payments and other remuneration taken into account when determining the base for calculating insurance premiums in terms of the author’s order agreement, the agreement on the alienation of the exclusive right to works of science, literature, art, the publishing license agreement, the license agreement on granting the right to use a work of science, literature, art, is defined as the amount of income received under an author's order agreement, an agreement on the alienation of the exclusive right to works of science, literature, art, a publishing license agreement, a license agreement on granting the right to use a work of science, literature, art, reduced by the amount actually produced and documented costs associated with the extraction of such income. If these expenses cannot be documented, they are accepted for deduction in the following amounts:

|

Name |

Cost standards (as a percentage of accrued income) |

|

Creation of literary works, including for theatre, cinema, stage and circus |

|

|

Creation of artistic and graphic works, photographs for printing, works of architecture and design |

|

|

Creation of works of sculpture, monumental and decorative painting, decorative and decorative art, easel painting, theatrical and film set art and graphics, made in various techniques |

|

|

Creation of audiovisual works (video, television and films) |

|

|

Creation of musical works: |

|

|

musical and stage works (operas, ballets, musical comedies), symphonic, choral, chamber works, works for wind orchestra, original music for film, television and video films and theatrical productions |

|

|

other musical works, including |

|

|

Performance of works of literature and art |

|

|

Creation of scientific works and developments |

|

|

Discoveries, inventions and creation of industrial designs (percentage of the amount of income received in the first two years of use) |

8. When determining the base for calculating insurance premiums, expenses confirmed by documents cannot be taken into account simultaneously with expenses within the established standard.

For reference:

Article 5. Payers of insurance premiums (Federal Law of July 24, 2009 N 212-FZ (as amended and supplemented, entered into force on January 3, 2014))

1. Payers of insurance premiums are policyholders determined in accordance with federal laws on specific types of compulsory social insurance, which include:

1) persons making payments and other remuneration to individuals:

a) organizations;

b) individual entrepreneurs;

c) individuals who are not recognized as individual entrepreneurs;

Law No. 212-FZ

ATTENTION!!!

The document lost force on January 1, 2017 due to the adoption of Federal Law dated July 3, 2016 No. 250 - FZ. At the same time, the Social Insurance Fund of the Russian Federation (hereinafter referred to as the Fund) continues to exercise control for the correctness of calculation, completeness and timeliness of payment (transfer) of insurance premiums payable to the Fund for reporting (calculation) periods expired before January 1, 2017, in the manner in force before the entry into force of this Federal Law (Article 20 of Law No. 250-FZ).

In accordance with Federal Law No. 212-FZ dated July 24, 2009 “On insurance contributions to the Pension Fund of the Russian Federation, the Social Insurance Fund of the Russian Federation, the Federal Compulsory Medical Insurance Fund,” the payer of insurance contributions is responsible for non-fulfillment or improper fulfillment of the obligations assigned to him by this Federal the law of obligations for the timely and full payment of insurance premiums, the timely submission and procedure for submitting established reports to the control body, as well as for refusal to submit or failure to submit to an official of the control body the documents necessary to monitor the payment of insurance premiums.

Failure to submit calculations for accrued and paid insurance premiums (Art.

46 of Law No. 212-FZ)

1. Failure by the payer of insurance premiums to submit calculations for accrued and paid insurance premiums to the body for control over the payment of insurance premiums at the place of registration within the deadline established by this Federal Law shall entail the collection of a fine in the amount of 5 percent of the amount of insurance premiums accrued for payment for the last three months of the reporting (calculated) ) period, for each full or partial month from the day established for its submission, but not more than 30 percent of the specified amount and not less than 1,000 rubles.

Payers of insurance premiums quarterly submit to the territorial body of the Social Insurance Fund of the Russian Federation at the place of their registration a calculation of accrued and paid insurance premiums (form 4-FSS), hereinafter referred to as the calculation, on paper no later than the 20th day of the calendar month following the reporting month period, and in the form of an electronic document - no later than the 25th day of the calendar month following the reporting period (clause 2, part 9, article 15 of Law No. 212-FZ),

2. Failure to comply with the procedure for submitting calculations of accrued and paid insurance premiums to the body monitoring the payment of insurance premiums in the form of electronic documents in cases provided for by this Federal Law shall entail a fine of 200 rubles.

Payers of insurance premiums, who have an average number of individuals in whose favor payments and other remunerations are made, for the previous billing period exceeds 25 people, as well as newly created (including during reorganization) organizations whose number of specified individuals exceeds this limit, submit calculations to the body for control over the payment of insurance premiums in the formats and in the manner established by the body for control over the payment of insurance contributions, in the form of electronic documents signed with an enhanced qualified electronic signature. Payers of insurance premiums and newly created organizations (including during reorganization), whose average number of individuals in whose favor payments and other remunerations are made for the previous billing period is 25 people or less, have the right to submit calculations in the form of electronic documents (Part 10, Article 15 of Law No. 212-FZ).

Non-payment or incomplete payment of insurance premiums

(Article 47 of Law No. 212-FZ)

1. Non-payment or incomplete payment of insurance premiums as a result of understating the base for calculating insurance premiums, other incorrect calculation of insurance premiums or other unlawful actions (inaction) of insurance premium payers shall entail a fine in the amount of 20 percent of the unpaid amount of insurance premiums.

2. Acts provided for in Part 1 of this article, committed intentionally, entail a fine in the amount of 40 percent of the unpaid amount of insurance premiums.

Refusal or failure to submit to the body monitoring the payment of insurance premiums the documents necessary to monitor the payment of insurance premiums (Article 48 of Law No. 212-FZ)

Refusal or failure by the payer of insurance premiums to submit documents (copies of documents) provided for by this Federal Law, or other documents necessary for monitoring the correctness of calculation, completeness and timeliness of payment (transfer) of insurance premiums, to the body monitoring the payment of insurance premiums, shall entail collection of a fine of 200 rubles for each document not submitted.

The official of the insurance premium control body conducting the inspection, has the right to request from the person being inspected the documents necessary for the inspection. The requirement to submit documents can be submitted to the head (authorized representative) of the organization or individual (legal or authorized representative) in person against signature, sent by registered mail or transmitted electronically via telecommunication channels. If the specified request is sent by registered mail, it is considered received after six days from the date of sending the registered letter. (Part 1, Article 37 of Law No. 212 - Federal Law).

12 August 2018 07:05 PM:: Federal Law of August 3, 2018 N 300-FZ “On Amendments to Article 5 of Part One and Articles 422 and 427 of Part Two of the Tax Code of the Russian Federation”

Federal Law of August 3, 2018 N 300-FZ "On Amendments to Article 5 of Part One and Articles 422 and 427 of Part Two of the Tax Code of the Russian Federation"

Adopted by the State Duma on July 26, 2018 Approved by the Federation Council on July 28, 2018 Article 1 Article 5 of the first part of the Tax Code of the Russian Federation (Collection of Legislation of the Russian Federation, 1998, No. 31, Art. 3824; 1999, No. 28, Art. 3487; 2001, N 53, Art. 5026; 2004, N 31, Art. 3231; 2006, N 31, Art. 3436; 2008, N 48, Art. 5519; 2013, N 30, Art. 4081; 2016, N 18, Art. 2506; N 22, Art. 3092; N 27, Art. 4176) add paragraph 4.2 as follows: "4.2. Provisions of acts of legislation on taxes and fees that change tax rates, insurance premium rates, tax benefits, the procedure for calculating taxes and insurance premiums , the procedure and deadlines for paying taxes and insurance premiums, introducing new taxes, insurance premiums for organizations or individual entrepreneurs who have received the status of a resident of a territory of rapid socio-economic development or the status of a resident of the free port of Vladivostok, in terms of legal relations related to the execution of an agreement on the implementation of activities, concluded in accordance with the Federal Law of December 29, 2014 N 473-FZ “On Territories of Rapid Socio-Economic Development in the Russian Federation” or the Federal Law of July 13, 2015 N 212-FZ “On the Free Port of Vladivostok”, do not apply until the end tax period for the relevant tax and (or) settlement period for insurance premiums, in which ten years have expired from the date the taxpayer (payer of insurance premiums) received the status of a resident of the territory of rapid socio-economic development or the status of a resident of the free port of Vladivostok, provided that such acts legislation on taxes and fees came into force after receiving the corresponding status." Article 2 Introduce into part two of the Tax Code of the Russian Federation (Collection of Legislation of the Russian Federation, 2000, N 32, Art. 3340; 2016, N 27, Art. 4176; N 49, Art. 6844; N 52, Art. 7497; 2017, N 1, Art. 16; N 49, Art. 7307, 7325; 2018, N 1, Art. 20; N 18, Art. 2565) the following changes: 1) subparagraph 7 of paragraph 1 of Article 422 shall be stated as follows: "7 ) the cost of travel of the employee to the place of use of the vacation and back and the cost of transporting luggage weighing up to 30 kilograms, as well as the cost of travel of non-working members of his family (husband, wife, minor children actually living with the employee) and the cost of transporting their baggage, paid by the payer of insurance premiums persons working and living in the regions of the Far North and equivalent areas, in accordance with the legislation of the Russian Federation, legislative acts of the constituent entities of the Russian Federation, decisions of representative bodies of local government, labor contracts and (or) collective agreements. In the case of taking a vacation outside the territory of the Russian Federation, the cost of travel or flights of the employee and non-working members of his family (including the cost of transporting luggage weighing up to 30 kilograms), calculated from the place of departure to the checkpoint across the State Border of the Russian Federation, is not subject to insurance premiums. including the international airport where the employee and non-working members of his family undergo border control at the checkpoint across the State Border of the Russian Federation;"; 2) in Article 427: a) paragraph 10 should be stated as follows: "10. The payers specified in subparagraph 11 of paragraph 1 of this article apply the reduced rates of insurance premiums provided for in subparagraph 5 of paragraph 2 of this article for ten years from the date they received the status of a participant in the free economic zone, starting from the 1st day of the month following the month, in which they received such status. The reduced rates of insurance premiums specified in subparagraph 5 of paragraph 2 of this article are applied to participants in a free economic zone that have received such status no later than within three years from the date of creation of the corresponding free economic zone. For payers who have lost the status of a participant in a free economic zone, the reduced rates of insurance premiums provided for in subparagraph 5 of paragraph 2 of this article do not apply from the 1st day of the month following the month in which they lost such status."; b) add paragraph 10.1 reads as follows: "10.1. The payers specified in subparagraphs 12 and 13 of paragraph 1 of this article apply the reduced rates of insurance premiums provided for in subparagraph 5 of paragraph 2 of this article for ten years from the date they received the status of a resident of the territory of rapid socio-economic development or the status of a resident of the free port of Vladivostok starting from the 1st day of the month following the month in which they received the corresponding status. Reduced rates of insurance premiums are applied by payers exclusively in relation to the base for calculating insurance premiums determined in relation to individuals employed in new jobs. For the purposes of this paragraph, a new workplace is understood to be a place created for the first time by a resident of the territory of rapid socio-economic development or a resident of the free port of Vladivostok in the execution of an agreement on the implementation of activities concluded in accordance with Federal Law of December 29, 2014 N 473-FZ “On Territories” rapid socio-economic development in the Russian Federation" or Federal Law of July 13, 2015 N 212-FZ "On the Free Port of Vladivostok" (hereinafter in this paragraph - the agreement on the implementation of activities). In this case, an individual employed in a new workplace is recognized as a person who has entered into an employment contract with a resident of the territory of rapid socio-economic development or a resident of the free port of Vladivostok and whose labor duties are directly related to the implementation of the agreement on the implementation of activities, including the operation of facilities fixed assets created as a result of the execution of an agreement on the implementation of activities. The federal executive body that, in accordance with Federal Law dated July 13, 2015 N 212-FZ "On the Free Port of Vladivostok", maintains the register of residents of the free port of Vladivostok, an organization recognized as a management company in accordance with Federal Law dated December 29, 2014 N 473 -FZ "On territories of rapid socio-economic development in the Russian Federation", a federal executive body authorized by the Government of the Russian Federation in accordance with Part 6 of Article 34 of the Federal Law of December 29, 2014 N 473-FZ "On territories of rapid socio-economic development" in the Russian Federation", submit to the tax authorities in the manner determined by the agreement on information exchange, information about the receipt and loss by the payer of insurance premiums of the status of a resident of a territory of rapid socio-economic development or the status of a resident of the free port of Vladivostok, as well as information about changes in the list of jobs payer related to new jobs. For payers who have lost the status of a resident of the territory of rapid socio-economic development or the status of a resident of the free port of Vladivostok, the reduced rates of insurance premiums provided for in subparagraph 5 of paragraph 2 of this article do not apply from the 1st day of the month following the month in which they lost corresponding status.

On the application of reduced tariffs in accordance with Federal Law dated July 24, 2009 No. 212-FZ

The reduced rates of insurance premiums specified in subparagraph 5 of paragraph 2 of this article are applied to a resident of a territory of rapid socio-economic development (with the exception of a resident of a territory of rapid socio-economic development located on the territory of the Far Eastern Federal District), who received such status no later than within three years from the date of creation of the corresponding territory of rapid socio-economic development. The reduced rates of insurance premiums specified in subparagraph 5 of paragraph 2 of this article are applied to a resident of a territory of rapid socio-economic development located in the Far Eastern Federal District, a resident of the free port of Vladivostok, who received the corresponding status no later than December 31, 2025, provided that that the volume of investments in accordance with the agreement on the implementation of activities is not less than: 500 thousand rubles - for a resident of the territory of rapid socio-economic development located in the Far Eastern Federal District; 5 million rubles - for a resident of the free port of Vladivostok." Article 3 1. This Federal Law comes into force on the date of its official publication, with the exception of Article 1 of this Federal Law. 2. Article 1 of this Federal Law comes into force on January 1, 2019 3. The provisions of paragraph 4.2 of Article 5 of the Tax Code of the Russian Federation (as amended by this Federal Law) apply to acts of legislation on taxes and fees that entered into force after January 1, 2019, and also apply to residents of territories of advanced socio-economic development, residents of the free port of Vladivostok, who received the corresponding status before January 1, 2019. 4. The effect of the provisions of paragraph 10.1 of Article 427 of the Tax Code of the Russian Federation (as amended by this Federal Law) in relation to residents of territories of rapid socio-economic development located on the territory of the Far Eastern Federal district, and residents of the free port of Vladivostok applies to legal relations arising from June 26, 2018. President of the Russian Federation V. Putin Moscow, Kremlin August 3, 2018 N 300-FZ

Legal Center IVV Ministry of Internal Affairs of Russia www.nashyprava.ru

Who makes what contributions to the Pension Fund? How are these funds distributed? These issues concern not only employers, but also individual entrepreneurs, as well as employees. That is, each of us, because the size of contributions to the Pension Fund directly determines the size of pensions in the future. It would be a good idea to check the reliability of your employer in terms of payment of contributions.

Who makes what contributions to the Pension Fund? How are these funds distributed? These issues concern not only employers, but also individual entrepreneurs, as well as employees. That is, each of us, because the size of contributions to the Pension Fund directly determines the size of pensions in the future. It would be a good idea to check the reliability of your employer in terms of payment of contributions.

Until 2010, a unified social tax was established in Russia. After 01/01/2010, instead of paying such a tax, mandatory contributions to state funds were introduced: Pension, social insurance, compulsory health insurance. Contributions are regulated by Federal Law No. 212-FZ of July 24, 2009, and contributions to the Pension Fund are also regulated by Law No. 167-FZ of December 15, 2001.

Who makes contributions to the Pension Fund and when?

Contributions to the Pension Fund represent the payment of insurance contributions for compulsory pension insurance. In turn, the latter term, in essence, means creating the prerequisites for ensuring a citizen’s right to a pension. That is, the state is taking measures (economic, legal, and organizational) to ensure pension payments in the future (from the concept of pension as compensation for earnings) - labor pension for old age, disability, loss of a breadwinner, funded pension, etc. At the same time, insurance premiums also provide payment of some social benefits (compensation for funerals) and fixed payments towards pensions (pension amounts).

The following are required to make contributions to the Pension Fund:

- organizations that make payments under labor and paid (for remuneration) civil contracts to individuals;

- individual entrepreneurs: for themselves and those persons to whom they paid money or otherwise paid for labor, work, services under any kind of contracts;

- individuals, if they have made payments under contracts and in the case where they are not individual entrepreneurs;

- lawyers, notaries and other categories of self-employed citizens (members of peasant farms) - as well as individual entrepreneurs.

That is, even in everyday life, if we use the services of another person, we are obliged to make contributions to the Pension Fund for such individuals.

Amount of contributions to the Pension Fund

Let’s immediately make a reservation that, unlike personal income tax, which is calculated based on the employee’s salary, bonuses, and regional coefficient, insurance contributions are not included in wages.

Article 8 of the Federal Law of July 24, 2009 No. 212-FZ

That is, the employee receives wages minus personal income tax. And in the Pension Fund of the Russian Federation, the payer also pays based on income, but does not withhold this amount directly from the salary.

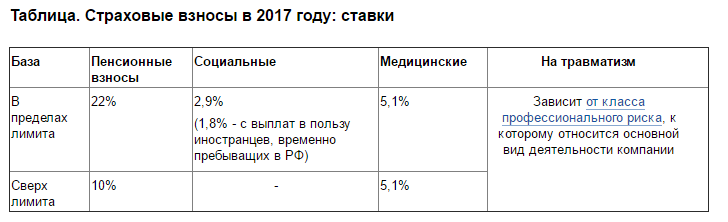

The actual amount of contributions to the Pension Fund depends on the category of the payer. For organizations that are subject to the general taxation regime, i.e. for most, in 2016 this amount will be 22%. And plus 10% if the size of the base (total income) is more than 796,000 rubles. This is for each employee. In 2017, this base will most likely change in accordance with the resolution of the Government of the Russian Federation adopted annually on this issue. The base is determined separately for each employee for each month from the beginning of deductions for him and on a cumulative basis.

Organizations under the simplified taxation system will pay 20%, like individual entrepreneurs, for each employee.

Additional tariffs for insurance contributions to the Pension Fund have been introduced for employers who have workplaces with hazardous and hazardous industries, i.e. in favor of persons entitled to a preferential pension. The tariff is determined based on the assessment of working conditions and the assigned class.

Deductions must be made by the 15th of each month (payment is for the previous month).

The self-employed population pays a fixed contribution to the Pension Fund for themselves. In 2016 it is 19,356.48 kopecks. + 1% from the amount of his income over 300,000 rubles. Such payment is made until December 31, 2016 by each individual entrepreneur, lawyer, private notary, etc.

How to check the amount of contributions to the Pension Fund

All contributions to the Pension Fund are reflected in the individual account of the insured. That is, your personal personal account. Remember that if a person decides to use a funded pension (which we wrote about in the corresponding article), then you can find out your pension savings using SNILS.

Pension contributions generated on an individual personal account can be found out through the government services portal, order a certificate on the Pension Fund website, or by contacting the Pension Fund in person at your place of residence. You must have SNILS and a passport with you. Another person can find out information only if they have the appropriate power of attorney.

When checking contributions to the Pension Fund, remember that currently 16% of contributions are taken into account on a personal account, and if a funded pension is formed - 10% on the insurance part and 6% on the funded part (in 2016, 16% is reflected for all employees due to with the “freezing” of the provisions of the law in this part).

The main document serving as guidance for the calculation and payment of mandatory contributions to extra-budgetary funds was Federal Law No. 212-FZ of July 24, 2009. Changes were periodically made to it regarding the procedure for carrying out the necessary calculations. This provision contained information about persons who are obliged to accrue and pay contributions to the Pension Fund of the Russian Federation, the Social Insurance Fund and the Federal Compulsory Medical Insurance Fund. At the beginning of 2017, a decision was made to cancel this document, which entailed a number of certain changes.

Federal Law-212: reasons for cancellation and partial effect

The main reason for canceling this document was the decision to transfer control over incoming contributions to the tax authority. This, in turn, abolished the settlement procedure that was prescribed in 212-FZ in connection with the payment of contributions for compulsory health insurance, compulsory medical insurance and other funds:

The decision to repeal this federal law eliminated the possibility of errors and confusion associated with the current procedure for submitting various forms of reporting and transferring funds to the Federal Tax Service.

Now control over the calculation of mandatory insurance contributions and the transfer of funds is carried out by the tax authority, and employees of the Pension Fund and Social Insurance Fund will check the correctness of accruals made in periods before 01/01/2017. In their work they will be guided by certain provisions of 212-FZ, including the edition that is currently in effect.

Get 267 video lessons on 1C for free:

Until all checks are completed, certain provisions of Federal Law-212 “On Insurance Premiums” will continue to apply.

How reporting will change due to the repeal of Law No. 212-FZ

According to the new reporting conditions, from the 1st quarter of 2017, calculations of insurance premiums will be provided not to the Pension Fund, but to the Federal Tax Service. It should be noted that this form will be completely new and, accordingly, all old provisions regarding the calculation and verification of the provided data will no longer be valid:

On the other hand, if the taxpayer needs to clarify the information provided in previous periods, then on his part it is necessary to transfer the calculation according to the old form to the Pension Fund of Russia branch where the enterprise was registered.

The updated calculation should be presented not just in the old form, but precisely in the form that was in effect during a specific period. In other words, the actions of Federal Law-212 will continue to apply to all clarifying and corrective reports submitted to the Pension Fund branches.

As for the coefficients and maximum bases for calculating contributions to the Pension Fund and the Social Insurance Fund, they will remain unchanged:

- for the Pension Fund - 796,000 rubles. with a tariff of 22% and 10% on the amount exceeding the base;

- for contributions to the Social Insurance Fund – 718,000 rubles. with a tariff of 2.9%, funds are not paid for amounts exceeding the base amount.

The installed bases will be indexed annually taking into account the level of wages. Contributions to the FFOMS will also be calculated at a rate of 5.1%, and for individual entrepreneurs the previous procedure for paying taxes will remain with an income limit of 300,000 rubles:

How will the procedure and deadlines for paying insurance premiums change?

Due to the fact that new reporting forms have been introduced, taxpayers and insured persons will have to be guided not by the provisions of 212-FZ, but by new recommendations and instructions when filling out these forms. These documents are freely available and can be downloaded on the official portal of the Federal Tax Service of the Russian Federation, as well as on the website of the Pension Fund of Russia. The new instructions provide examples of calculating this or that indicator, and indicate various nuances and features of filling out new documentation forms.

An important indicator is the reporting deadline. New forms of documentation have different submission deadlines. Accruals must be paid, as before, by the 15th day of the next period, and instead of forms RSV-1 and 4-FSS, policyholders will be required to submit a single calculation to the Federal Tax Service for all contributions. Deadline for its provision:

- in paper form - until the 20th day of the month following the reporting month;

- in electronic form - until the 25th day of the month following the reporting month.

Tax inspectors will now check the accuracy of information, and information about length of service will be checked by employees of the Pension Fund of the Russian Federation. To eliminate the possibility of receiving fines and penalties, as well as problems associated with late or incorrect completion of a specific form, you should carefully study the detailed instructions and keep in mind that the old 212-FZ “On Insurance Contributions to the Pension Fund of the Russian Federation” will only be valid in limited cases.

the federal law

"On insurance contributions to the Pension Fund of the Russian Federation, the Social Insurance Fund of the Russian Federation, the Federal Compulsory Medical Insurance Fund and territorial compulsory medical insurance funds"

the federal law

"On amendments to certain legislative acts of the Russian Federation and the recognition as invalid of certain legislative acts (provisions of legislative acts) of the Russian Federation in connection with the adoption of the Federal Law "On insurance contributions to the Pension Fund of the Russian Federation, the Social Insurance Fund of the Russian Federation, the Federal Compulsory Medical Fund insurance and territorial compulsory health insurance funds" *1

_____

*1 Continued. Beginning see "NV: Comments..." N 9"2009 and N 10"2009 .

Full texts of official documents are available in electronic form to subscribers of the online version.

A comment

E.A. Kotko,

leading expert of the Association of Accountants,

auditors and consultants"

In this issue we will continue to comment on the laws adopted in July 2009 that establish the payment of insurance contributions to state extra-budgetary funds starting next year.

Payments not subject to insurance premiums

Let's look at how the list of payments not subject to insurance contributions has changed compared to payments not subject to the unified social tax until the end of 2009. Payments for which insurance premiums are not charged are given in

Art. 9 of Law N 212-FZ *1. Until the end of 2009, amounts not subject to UST are regulated by

Art. 238 Tax Code of the Russian Federation . The provisions of these articles largely repeat each other, but there are some differences that should be noted.

_____

*1 Full name of the document - Federal Law of July 24, 2009 N 212-FZ “On insurance contributions to the Pension Fund of the Russian Federation, the Social Insurance Fund of the Russian Federation, the Federal Compulsory Medical Insurance Fund and territorial compulsory medical insurance funds” (hereinafter referred to as Law N 212-FZ).

Payments related to the dismissal of employees

According to subp. 2 "d" clause 1 art. 9 of Law N 212-FZ All types of compensation payments established by the legislation of the Russian Federation, legislative acts of the constituent entities of the Russian Federation, decisions of representative bodies of local self-government (within the limits established in accordance with Russian legislation) related to the dismissal of employees, with the exception of compensation for unused vacation, are not subject to insurance contributions.

***

Note!

From January 1, 2010, compensation amounts for unused vacations are subject to insurance contributions. The specified amounts were not subject to UST (

subp. 2 p. 1 art. 238 Tax Code of the Russian Federation ).

***

Example

Taxation of payments upon dismissal in 2009 and 2010

An employee resigns due to conscription for military service.(clause 1, part 1, article 83 of the Labor Code of the Russian Federation) . According to labor legislation, he is paid severance pay ( Art. 178 Labor Code of the Russian Federation ) in the amount of 11,230 rubles. and compensation for unused vacation ( Art. 127 Labor Code of the Russian Federation ) in the amount of 4600 rubles. In addition, the employee was accrued wages for days worked in the month of dismissal - 12,000 rubles.

What is the tax treatment for these payments if the employee quits in 2009 and if he quits in 2010?

Situation 1

Let's say the employment contract with the employee was terminated on December 22, 2009. On the same day the final payment was made to him.

Valid as of December 22, 2009 Ch. 24 of the Tax Code of the Russian Federation, and according to sub. 2 p. 1 art. 238 Tax Code of the Russian Federation All types of compensation payments (within the limits determined in accordance with the legislation of the Russian Federation) established by federal legislation, legislative acts of constituent entities of the Russian Federation, decisions of representative bodies of local self-government, incl. payments related to the dismissal of employees, including compensation for unused vacation.

Thus, only the amount of wages accrued to the employee for the days worked during the months of dismissal will be included in the taxable base for the Unified Social Tax. Severance pay and compensation for unused unused vacation will not be subject to unified social tax.

Situation 2

Let's say an employee quits on January 22, 2010. On the same day the final payment was made to him.

Since January 22, 2010 Ch. 24 Tax Code of the Russian Federation no longer valid, but comes into force Law N 212-FZ. According to sub. 2 "e" clause 1 art. 9 of this Law Insurance premiums are not subject to all types of compensation payments (within the limits determined in accordance with the legislation of the Russian Federation) established by federal legislation, legislative acts of constituent entities of the Russian Federation, decisions of representative bodies of local self-government, incl. payments related to the dismissal of employees, with the exception of compensation for unused vacation.

Thus, the taxable base for insurance premiums does not include only the amount of severance pay accrued in accordance with Art. 178 Labor Code of the Russian Federation . The amount of wages accrued to the employee for days worked during the months of dismissal and (please note!) compensation for unused vacation are subject to insurance contributions from January 1, 2010.

Payments related to the employment of employees dismissed due to measures to reduce numbers or staff, reorganization or liquidation (termination of activities)

According to subp. 2 "z" clause 1 art. 9 of Law N 212-FZ Compensation payments established by law related to the employment of workers dismissed due to:

- implementation of measures to reduce the number or staff, reorganize or liquidate the organization; - termination by individuals of activities as individual entrepreneurs, termination of powers by notaries engaged in private practice, and termination of the status of a lawyer; - termination of activities by other individuals whose professional activities in accordance with federal laws are subject to state registration and (or) licensing. Until December 31, 2009 according to subp. 2 p. 1 art. 238 Tax Code of the Russian Federation Unified social tax is not subject to compensation payments to employees dismissed due to measures to reduce numbers or staff, reorganization or liquidation of the organization. Thus, the list of persons who may not include in the taxable base compensation payments related to the employment of workers dismissed for certain reasons has expanded. They are not subject to insurance premiums if they are paid by any employers (all persons making payments to individuals), and not just organizations (as stated earlier for UST).Payments related to the performance of work duties by an individual, incl. moving to work in another area

INit is stated that all types of compensation payments established by the legislation of the Russian Federation, legislative acts of the constituent entities of the Russian Federation, decisions of representative bodies of local self-government (within the limits of the norms established in accordance with Russian legislation) related to the performance of labor duties by an individual, including h. in connection with moving to work in another area, with the exception of:

- payments in cash for work under difficult, harmful and (or) dangerous working conditions, except for compensation payments in an amount equivalent to the cost of milk or other equivalent food products;

- payments in foreign currency in lieu of daily allowances made in accordance with the legislation of the Russian Federation by Russian shipping companies to crew members of ships sailing abroad, as well as payments in foreign currency to crew members of Russian aircraft operating international flights.

A similar norm contains subp. 2 p. 1 art. 238 Tax Code of the Russian Federation : Compensation payments established by the relevant legislation related to the performance by an individual of labor duties (including moving to work in another area and reimbursement of travel expenses) are not subject to UST. Thus, this item in the list of non-taxable amounts ( subp. 2 "i" clause 1 art. 9 of Law N 212-FZ compared with subp. 2 p. 1 art. 238 Tax Code of the Russian Federation ) is supplemented by an indication of compensation payments related to the performance of work duties, which are an exception to non-taxable payments (i.e. in 2010 they will be subject to insurance contributions). For the unified social tax, such exceptions in Tax Code of the Russian Federation not provided. The procedure for imposing insurance premiums on travel expenses of employees is described (separately from compensation payments) in clause 2 art. 9 of Law N 212-FZ . There have been no fundamental changes in the taxation of travel expenses.

Financial assistance to employees

According to subp. 3 "c" clause 1 art. 9 of Law N 212-FZ The amounts of one-time financial assistance provided by insurance premium payers to employees (parents, adoptive parents, guardians) at the birth (adoption) of a child, paid during the first year after birth (adoption), but not more than 50,000 rubles, are not subject to insurance contributions. for each child.

Thus, from January 1, 2010, the period during which financial assistance must be paid to employees (parents, adoptive parents, guardians) at the birth (adoption) of a child is limited, so that it is not subject to insurance contributions. This period is one year from the date of birth of the child. If this financial assistance is provided at a later date, it will be subject to insurance contributions in accordance with the general procedure. According to subp. 11 clause 1 art. 9 of Law N 212-FZ Amounts of financial assistance provided by employers to their employees not exceeding 4,000 rubles are not subject to insurance contributions. per employee per billing period. Previously, only amounts of material assistance paid to individuals from budget sources by organizations financed from budget funds, not exceeding 3,000 rubles, were not subject to UST. per individual per tax period ( subp. 1 clause 1 art. 238 Tax Code of the Russian Federation ).

So, the number of non-taxable payments includes amounts of financial assistance (not exceeding 4,000 rubles per employee per billing period) provided by any employers to their employees, and also the circle of persons who can be provided with financial assistance not subject to insurance contributions has been expanded, and the maximum non-taxable amount has been increased. amount of financial assistance.

Amounts of insurance payments for various types of employee insurance

In addition to the payments specified in subp. 7 clause 1 art. 238 Tax Code of the Russian Federation , V subp. 5 p. 1 art. 9 of Law N 212-FZ Among the payments not subject to insurance contributions are:

- the amount of payments (contributions) of the payer of insurance premiums under contracts for the provision of medical services to employees, concluded for a period of at least one year with medical organizations that have licenses to provide medical services, issued in accordance with the legislation of the Russian Federation;

- the amount of pension contributions of the payer of insurance premiums under non-state pension agreements.

Thus, the list of insurance payments (contributions) paid under insurance contracts for employees not subject to insurance premiums has been expanded (compared to the Unified Social Tax).

Insurance premium rates

Insurance contributions to state extra-budgetary funds will be paid on a flat scale, and not on a regressive scale, as was established for the unified social tax.

Moreover, according to Art. 57 Law No. 212-FZ for 2010 (and for certain categories of insurance premium payers for 2011-2014), a transition period is established, during which insurance rates will be lower than in 2011 and subsequent years. The list of these insurance premium payers and the rates they apply were published in No. 9, 2009 of the magazine “NV: Comments on Regulatory Documents for Accountants.” Separate attention should be paid to the calculation of insurance premiums payable to the Pension Fund of the Russian Federation (PFR).

According to clause 3 art. 1 of Law N 212-FZ The specifics of paying insurance premiums for each type of compulsory social insurance are established by federal laws on specific types of compulsory social insurance*1. In particular, the specifics of payment of insurance contributions to the Pension Fund for compulsory pension insurance are regulated

Federal Law of December 15, 2001 N 167-FZ "On Compulsory Pension Insurance in the Russian Federation" (edited) Federal Law of July 24, 2008 N 213-FZ ) (Further - Law N 167-FZ ). As follows from the provisions

Art. 33 Law No. 167-FZ , insurance premiums payable to the Pension Fund will be calculated and paid separately to finance the insurance and funded parts of the pension. At the same time, for persons born in 1966 and older, all insurance contributions payable to the Pension Fund will be paid to finance the insurance part of the pension; for persons born in 1967 and younger - 6% of the tariff established for the Pension Fund of Russia will constitute the funded part, the remaining interest (for ordinary payers*2 is 14%, i.e. 20% - 6%) - the insurance part of contributions paid in Pension Fund (see Table 1 on p. 70). Starting from 2011, the size of insurance tariffs will increase compared to the tariffs established for 2010, and all organizations and individual entrepreneurs making payments and other remuneration to individuals, except for certain categories of payers, for whom a long grace period is established, extending to 2011-2014 years, will pay insurance premiums according to the tariffs specified in

clause 2 art. 12 of Law N 212-FZ (see commentary in No. 9 "2009 of the magazine "NV: comments on regulatory documents for accountants") Insurance tariffs in the Pension Fund of the Russian Federation (broken down into the insurance and savings part) for such payers of insurance premiums are given in Table 2 (see on p. 72).

_____

*1 In addition, for uniform application purposes

Law N 212-FZ Since January 1, 2010, the Ministry of Health and Social Development of Russia has been granted the right to issue appropriate clarifications (see.

Decree of the Government of the Russian Federation dated September 14, 2009 N 731 ).

*2 In other words, payers of insurance premiums for whom lower rates are not established (see page 1 of the table on p. 70).

Table 1

Reduced rates of insurance premiums payable to the Pension Fund in 2010

|

N p/p |

Tariff stra- hovoy |

To finance the insurance part of the labor pension, % |

To finance the savings |

base |

||

|

contribution, % |

for persons born in 1966 and older |

for persons born in 1967 and younger |

labor pension, % | |||

|

1

|

All payers except those listed below |

20

|

20

|

14

|

6

|

Clause 1 of Art. 33 of Law N 167-FZ (as amended by Law N 213-FZ) |

|

2

|

Agricultural producers meeting the criteria specified in Art. 346.2 Tax Code of the Russian Federation (except for organizations and individual entrepreneurs applying the single agricultural tax); Organizations of folk arts and crafts; Family (tribal) communities of indigenous peoples of the North engaged in traditional economic sectors |

15,8

|

15,8

|

9,8

|

6

|

Subp. 1 item 2 art. 33 of Law N 167-FZ (as amended by Law N 213-FZ) |

|

3

|

Organizations and individual entrepreneurs that have resident status of a technology-innovation special economic zone and make payments to individuals working in the territory of a technology-innovation special economic zone; Organizations and individual entrepreneurs using a simplified taxation system; Organizations and individual entrepreneurs paying UTII (in relation to payments and other remuneration made to individuals in connection with conducting business activities subject to UTII); Payers of insurance premiums making payments and other remunerations to individuals who are disabled people of groups I, II or III - in relation to the specified payments and remunerations; Public organizations of disabled people (including those created as unions of public organizations of disabled people), among whose members disabled people and their legal representatives make up at least 80%, their regional and local branches*1; Organizations whose authorized capital consists entirely of contributions from public organizations of disabled people and in which the average number of disabled people is at least 50%, and the share of wages of disabled people in the wage fund is at least 25%*1; Institutions created to achieve educational, cultural, medical and recreational, physical culture, sports, scientific, information and other social goals, as well as to provide legal and other assistance to people with disabilities, disabled children and their parents (other legal representatives), the sole owners of property which are public organizations of disabled people*1 |

14

|

14

|

8

|

6

|

Subp. 2 p. 2 art. 33 of Law N 167-FZ (as amended by Law N 213-FZ) |

|

4

|

Organizations and individual entrepreneurs applying the Unified Agricultural Tax (Unified Agricultural Tax) |

10,3

|

10,3

|

4,3

|

6

|

Subp. 3 p. 2 art. 33 of Law N 167-FZ (as amended by Law N 213-FZ) |

|

_____ |

||||||

table 2

Reduced rates of insurance premiums payable to the Pension Fund in 2011-2014 for certain categories of payers*1 (clauses 4 and 5 of Article 33 of Law No. 167-FZ )

_____

*1 For a list of these insurance premium payers, see p. 71.

|

Period |

Insurance tariff |

To finance the insurance part of the labor pension, % |

|

|

|

contribution, % |

|

|

labor pension, % for persons born in 1967 and younger |

|

|

2011-2012 |

16

|

16

|

10

|

6

|

|

2013-2014 |

21

|

21

|

15

|

6

|

Certain categories of insurance premium payers for whom their reduced tariffs are established during the transition period of 2011-2014 include organizations and individual entrepreneurs specified in clause 1 art. 58 Law No. 212-FZ Andclause 4 art. 33 Law No. 167-FZ:

- agricultural producers meeting the criteria specified in Art. 346.2 Tax Code of the Russian Federation ;

- organization of folk arts and crafts;

- family (tribal) communities of indigenous peoples of the North engaged in traditional economic sectors;

- organizations and individual entrepreneurs with resident status of a technology-innovation special economic zone and making payments to individuals working in the territory of a technology-innovation special economic zone;

- organizations and individual entrepreneurs using the Unified Agricultural Tax;

- payers of insurance premiums making payments and other remunerations to individuals who are disabled people of group I, II or III - in relation to these payments and remunerations;

- public organizations of disabled people (including those created as unions of public organizations of disabled people), among whose members disabled people and their legal representatives make up at least 80%, their regional and local branches*1;

_____

clause 1 art. 58 Law No. 212-FZ ).

- organizations whose authorized capital consists entirely of contributions from public organizations of disabled people and in which the average number of disabled people is at least 50%, and the share of wages of disabled people in the wage fund is at least 25%*1;

_____

*1 With the exception of insurance premium payers engaged in the production and (or) sale of excisable goods, mineral raw materials, other minerals, as well as other goods in accordance with the list approved by the Government of the Russian Federation upon submission of all-Russian public organizations of disabled people (

clause 1 art. 58 Law No. 212-FZ ).

- institutions created to achieve educational, cultural, medical and recreational, physical culture, sports, scientific, information and other social goals, as well as to provide legal and other assistance to people with disabilities, disabled children and their parents (other legal representatives), the sole owners whose property is public organizations of disabled people*1.

_____

*1 With the exception of insurance premium payers engaged in the production and (or) sale of excisable goods, mineral raw materials, other minerals, as well as other goods in accordance with the list approved by the Government of the Russian Federation upon submission of all-Russian public organizations of disabled people (

clause 1 art. 58 Law No. 212-FZ ).

In 2011-2014, these payers apply the insurance premium rates given in clause 2 art. 58 Law No. 212-FZ (tariffs are given in the commentary published in N 9 "2009 of the magazine "NV: comments on regulatory documents for accountants"). The appropriate breakdown of pension contributions into the insurance and funded parts is established pp. 4And5 tbsp.33 Law No. 167-FZ(see Table 2).

Note. The period 2011-2014 is no longer preferential for the following payers (i.e. they pay insurance premiums at generally established rates):

- payers of insurance premiums specified in table. 1;

- organizations and individual entrepreneurs using the simplified tax system;

- organizations and individual entrepreneurs paying UTII.

All payers of insurance premiums starting from 2015 (and the payers listed in the note to Table 2 - already from 2011) will have to apply the tariffs established in

clause 2 art. 12 of Law N 212-FZ (tariffs are given in the commentary published in N 9 "2009 of the magazine "NV: comments on regulatory documents for accountants"). At the same time, insurance contributions to the Pension Fund of the Russian Federation will be calculated separately to finance the insurance and funded parts of the labor pension according to the tariffs established in

clause 2.1*1 art. 22 of the Law of December 15, 2001 N 167-FZ(see Table 3).

_____

*1 Provisions clause 2.1 art. 22 Law No. 167-FZ

come into force on January 1, 2011 (see.

subp. "b" clause 19 of Art. 27 ,

clause 4 art. 41 of the Law of July 24, 2009 N 213-FZ) .

Table 3

Tariffs of insurance premiums payable to the Pension Fund of the Russian Federation, applied by individual policyholders since 2011 and by all policyholders since 2015 (clause 2.1 of article 22 of Law No. 167-FZ

)

|

Insurance tariff |

To finance the insurance part of the labor pension |

To finance the funded part |

|

|

contribution |

for persons born in 1966 and older |

for persons born in 1967 and younger |

labor pension for persons born in 1967 and younger |

|

26%

|

26%

|

20%

|

6%

|

(To be continued)

Insurance premiums were paid to the Pension Fund and the Social Fund. and honey insurance according to the rules and conditions prescribed in Federal Law 212. On January 1, 2017, the law on insurance contributions to the Pension Fund lost its force and this area began to be regulated by Chapter 34 of the Tax Code of the Russian Federation. But some provisions of Federal Law 212 are still in use and are relevant for citizens.

What is Federal Law 212?

The law on insurance contributions to the Pension Fund was adopted by the State Duma on July 17, 2009, and approved by the Federation Council the next day, July 18, 2009. The latest changes took effect on December 19, 2016. But on January 1, 2017, Federal Law 212 lost its force. This law regulated all payments to state insurance authorities and legal relations between employees of insurance organizations that control payment and citizens. It contains 8 chapters and 62 articles.

- The first chapter describes all the general provisions of the law, including concepts and definitions of these concepts. It describes what an organization, individual and individual entrepreneur are in the field of insurance premiums, describes banks, accounts, the connection of contributions with place of residence and work, etc. This chapter lists the bodies that have the right to control and receive insurance premiums from citizens, conduct recording them, determining deadlines;

- Year 2 details the premium payment process, admissions and forms. Who is the payer, how accounting occurs, the essence of the base and the calculation of monetary amounts for each type of person. Which period of the financial year is the calculation period and which period is the reporting period. Tariffs, dates, procedures for calculations and recalculations and methods for making changes to the information provided to organizations;

- The third describes ways of fulfilling the duties of payers, organizations accepting payments, employees of these bodies, methods of monitoring the timeliness of payments and the quality of work of the bodies;

- Chapter number four provides a detailed list of the rights and obligations of the parties;

- The fifth describes payment control, how inspections and visits are carried out, what documents are required, how this is completed and who has access to information about payers;

- In the sixth year, situations are formalized in which the parties are responsible for their actions and penalties. It also describes situations of insurmountable gravity and force majeure, in which the parties are allowed not to comply with the law;

- The seventh describes methods of appealing against acts or actions of authorities, as well as forms and applications for appeal;

- Chapter number eight contains all the final provisions, conditions, amendments to the law, etc.

After the repeal of Federal Law 212 on insurance contributions to the Pension Fund, information about this area can only be found in the Tax Code of the Russian Federation, in chapter number 34.

New amendments

The latest revision of Federal Law 212 occurred on December 19, 2016, with the adoption of Federal Law No. 438. According to these changes, after the words “in accordance with the Federal Law “On the development of the Crimean Federal District and the free economic zone in the territories of the Republic of Crimea and the federal city of Sevastopol”” were added the words “and the free economic zone in the territories of the Republic of Crimea and the federal city of Sevastopol.”

Article seven was last revised in 2015. It describes the objects of taxation of insurance of citizens. These objects, by law, are considered to be payments and rewards received by individuals from payers in labor relations or during transactions with civil contracts. The objects are not payments in cases where, during a civil contract, property passes into the possession of another person.

Article eight describes the basis in which the accrual of insurance payments by citizens to the Pension Fund of the Russian Federation is kept. This article was last updated in 2014. It states the amount of payments, for what it was paid, and the billing period. Payers determine the base for each individual separately.

The ninth describes situations when payers pay individuals amounts that are not subject to insurance premiums:

- State benefits;

- Remuneration under copyright contracts for stateless persons or foreign persons;

- Cash amounts for clothing or food supplies and others received by military personnel;

- If organizations pay employees money to pay interest on loans or to build housing;

- Any amounts for education under professional programs;

- Amounts of assistance from managers to employees, but not more than 4,000 rubles;

- Cash for employees with benefits in public transportation;

- All payments of compensation by Russian authorities;

- The cost of special clothing that is issued to employees according to safety rules in accordance with the legislation of the Russian Federation;

- Any income, other than wages, of registered residents of small peoples of the North;

- Any amounts paid to all individuals who participated and assisted during election processes, etc.

11th century describes how dates for payments are determined. In general, the parties independently decide in whose favor the date is chosen. Usually the date is determined in favor of the employee or individual. Since the publication of this article in the law, it has never been changed.

Article 14 of the described law regulates all deductions and their amount. The latest amendments to this article were made to the law in 2014. According to these changes, payers do not pay insurance premiums during periods of conscription military service, caring for a child of one parent until the age of one and a half years, caring for a disabled person of group 1, the period of cohabitation of spouses when one of them performs military service, the period of cohabitation of spouses abroad during business trips.

The calculation procedure is regulated by Article 15 of Federal Law 212 and the last changes to the article were made in 2015. The changes apply to separate divisions of legal entities. Such divisions are opened by legal entities with bank accounts, through which they fulfill the obligations and main responsibilities of organizations regarding insurance premiums.

19 was drawn up with a procedure for paying arrears; the last changes were made to it in 2014. Under this change, forms and applications are regulated by a special body that controls the payment of insurance premiums.

On January 1, 2015, during changes to the law and a new edition, Article 44 lost its force. But then there were changes in Art. 58, which regulates the list of persons who are entitled to reduced rates or discounts. According to the changes, reduced tariffs are provided to employees paying remuneration to the crew of ships, excluding ships transporting or trading oil. According to the same changes, reduced rates are provided to participants of non-profit organizations engaged in education, scientific research, culture and art.

In 2017, the law was repealed and lost its force on January 1st.

Download the current edition of 212 Federal Law

212 of the Federal Law on insurance contributions to the Pension Fund of the Russian Federation was repealed, so its current version cannot be downloaded. However, many provisions are still used by the Government of the Russian Federation and state bodies regulating insurance payments in the Tax Code, Chapter 34. Therefore, this law can still be useful to citizens and employees of insurance organizations.

You can download Federal Law 212 “On Insurance Contributions to the Pension Fund” of the Russian Federation