Let's learn to be financially independent with Cash Flow. How to start cash flow and let wealth into your life Visualization “Money Magnet”

Learning to subjugate money energy is the most difficult thing. But the most interesting thing is that having mastered this most dense material energy, it will become much easier to work with other energies. First you need to understand that the energy of prosperity is the same energy of creativity, love, sex, pleasure and abundance. Throw out of your head thoughts like “I’m happy in love, so I’m unlucky with money” and vice versa - “everything is fine with finances, that’s why everyone is using me, there’s no love.” The energy of prosperity will most quickly come to you by the hand with love. It is important for men to always remember that wealth comes through his love for a woman, giving gifts and caring. An unkind woman will “prevent” her man from reaching the top. And women should try to remember that wealth will come to the family faster through her sense of self, the ability to enjoy herself. If a woman doesn’t have a man now, then she all the more needs to quickly learn to love herself, pamper and dress herself up, and give herself emotional release. It also happens that there is a man, but “it’s as if he’s not there.” It's sad, but this is not uncommon. And the woman takes on male responsibilities - from an inspirer she turns into a breadwinner. Such a woman should still try to pay more attention to the development of feminine qualities in herself, and not devote energy to trying to re-educate her half. Why is it important to regulate the relationship between a man and a woman on the path to prosperity? Because imbalances in relationships directly affect the reality in which we live. Dissatisfaction with a partner automatically makes us dissatisfied with material reality. When relationships improve, other things also stabilize.

Another thing you should always remember is that money does not tolerate people worrying about it. The surest and fastest way to become very poor and unhappy is to constantly worry that you won't have enough. Even if the situation in which you find yourself is complex and requires an immediate solution, even then you should not waste your energy on worries. You need to calmly solve the problem, if possible, or simply switch to other thoughts and things. This is quite difficult to learn, because from childhood we learn to worry about everything - they will punish you, they will give you a bad mark, etc., but having mastered this method, you will receive a magic wand for solving problems. This method will not bring millions, but there will be fewer problems with money.

If you do not want to be content with little, then first of all you need to expand your internal financial horizons. Calculate your average monthly income over the last year - this is your real framework. This is your financial ceiling for today. Don't be afraid to ask the Universe for more than you currently receive. Write down what you want to spend the money on. By not being lazy about writing down your material desires, you can already double your cash flow.

Remember, money comes for a specific purpose - dinner at a restaurant, a new dress, English courses, a trip to Tunisia or charity, or maybe you have a big dream? For the Universe, all dreams, plans and goals are equivalent. Don't worry about the scale of your dreams, but don't neglect the small details either.

Another secret is the law of tithing. Give 10% of your income monthly to charity. Check for yourself how it works.

For those who are engaged in the development of spirituality and self-improvement, you first of all need to improve the material side of life. Without a solid material foundation, you will inevitably turn back in your development. If they tell you that money is not the main thing or that it is evil, then run away from these sages to distant lands. Unless, of course, you have already grown to Christ consciousness.

Net cash flow is one of the main indicators of business performance, designed to answer the management question “Where is the money?” Read what this indicator is, what components it is formed from and how to calculate it. And also see an example of calculating net cash flow.

What is this article about?:

What is net cash flow

Net cash flow (NCF) is the result of summing up all cash inflows and cash outflows (minus) for a project over time intervals, usually months or years. The indicator is used to calculate the economic efficiency of an investment project, as well as preparing a company cash flow statement for the past period.

The inflow and outflow of capital - this is the receipt and repayment of loans and borrowings, the payment of dividends to shareholders - are not used in calculating the NPV for an investment project, because otherwise the picture of the investment attractiveness of the project will be distorted.

Net Cash Flow Formula

Before we talk about how to find net cash flow, let's look at what it consists of. NPV includes:

- Operating Cash Flow (OCF).

- Cash flow from financing activities (FCF).

- Cash flow from investing activities (ICF).

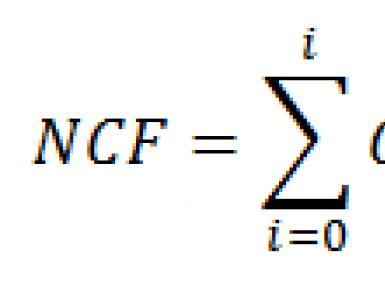

Therefore, net cash flow is determined by the formula:

where i is a time interval, usually a month or a year

The division of cash flow into operating, financial and investment carries an important meaning. Having received the overall result in the form of cash flow, you will find it difficult to answer which of the company's areas of activity had a positive (or negative) effect on the change in cash flow.

Are operating activities unprofitable? Or does this high level of debt have a negative effect in the form of large amounts of interest payments? Or did the company invest in a new project or purchase new equipment during the reporting period? By dividing your cash flow into its components, you will clearly see all the trends in your business and draw the right conclusions.

Let us visualize the cash flows belonging to each component.

Drawing. Components of net cash flow

Depending on the specific situation, the same cash flows may relate to different types of activities. For example, interest on a loan can be both a financial activity, if the loan is taken to finance an ongoing business, and an investment activity, if the loan is spent only on a new line of business. Leasing payments can also be either an operating cash flow or a financial or investment cash flow.

Users of net cash flow information

The company provides information about net cash flow in the cash flow statement (cash flow statement). It belongs to regulated reports, because its importance is difficult to overestimate. The cash flow statement collects all the information about changes in a company's cash during the reporting period.

For company management, net cash flow is company liquidity management tool . That is, based on the cash flow statement data, managers can assess whether the company will be able to pay off accounts payable, whether there will be enough funds to invest in new projects, or, on the contrary, it is necessary to look for ways to externally finance activities.

The cash flow statement provides creditors and investors with a basis for making investment decisions, showing how well a company can manage cash, whether it will pay dividends, and so on.

Methods for calculating net cash flow

To calculate net cash flow and complete the cash flow statement, you can use the direct or indirect method. The choice of the calculation method that suits you depends on the current accounting in your company, on the completeness of the initial data on income and expenses and on your goals, of course.

Direct method

The method is based on the direct use of company cash account data. To use it, it is necessary to carry out preparatory measures, that is, set up an accounting analyst system for the “bank” and “cash” accounts.

- Fill out the activity guide. Bring in operating activities, financing activities, investing activities.

- Fill out the directory of cash flow items, adding all the items you need to account for.

- Assign each cash flow to an activity type, a cash inflow item, or a cash outflow item.

As a result, at the end of the reporting period, you will receive net cash flow, presented in the form of a cash flow statement using the direct method.

It will look as shown in Table 1.

Table 1. ODDS example (fragment)

The advantages of this method are:

- the ability to show the sources of cash inflow and cash outflow, conduct analytics on counterparties, contracts, nomenclature, etc.;

- direct link to the cash flow budget and easy plan-factual analysis;

- ease of building a payment calendar based on data.

The direct method also has disadvantages, they are as follows:

- labor intensity. If the company uses the direct method of accounting for DDS, then local performers need to fill out at least two additional analytics for each movement. For large volumes, this is a catastrophic amount of labor hours;

- Based on the cash flow statement generated by the direct method, it is impossible to determine the relationship between the financial result and changes in the volume of funds.

Indirect method

The indirect method is considered simpler for calculating net cash flow, although international reporting standards recommend using the direct method. In order to calculate the NPV using the indirect method, you only need to have detailed data on the accrual of the company’s income and expenses for the reporting period.

You need to act according to the algorithm:

- Take the company's statement of financial position and statement of comprehensive income for the period.

- Create the structure of the ODDS, for example, in Excel, as shown in Table 2.

table 2

- Fill out the report sequentially, subtracting (adding) non-monetary transactions related to operating activities from the amount of the net financial result.

Such operations include:

- depreciation of fixed assets and intangible assets;

- income/loss from disposal of fixed assets and intangible assets;

- income/loss from revaluation of fixed assets and intangible assets;

- income tax expenses;

- income/loss from currency revaluation;

- creation / write-off of reserves;

- writing off bad debts.

As a result, you will receive net cash flow from operating activities.

- Next, enter into the table positive and negative cash flows from financial activities, such as:

- obtaining loans;

- loan repayment;

- finance lease obligations;

- contributions to share capital.

The result will be net cash flow from financing activities.

- Finally, enter all cash transactions of an investment nature, such as:

- acquisition of fixed assets, intangible assets, financial non-current assets;

- sale of non-current assets;

- receiving dividends;

- loans provided and interest on them.

Thus, you will form a net profit margin from investment activities.

- The last step will be summing up the cash flows and obtaining an indicator calculated by the indirect method.

The advantages of using the indirect method include:

- Quick and easy filling of ODDS.

- The ability to clearly see the sources of cash flow generation and identify reserves for its optimization.

Disadvantages of the indirect method:

- Based on it, it is impossible to create a cash flow budget.

- It will be difficult for a non-financier to understand and analyze.

When using both direct and indirect methods, it is necessary to check the change in funds for the period. Check what the net cash flow is equal to, is the equality true?

NDP = DS end.p - DS start.p

If yes, then you filled out the ODDS correctly.

Example of calculating net cash flow

Net cash flow is used not only for the statement of cash flows for the past period. It is a key parameter of investment planning. All investment indices and parameters are calculated based on this indicator. Let's look at an example of how to form the NPV of an investment project and avoid common mistakes.

A company operating in the digital mobile equipment wholesale market is considering an investment project to open a network of retail sales points in Moscow and St. Petersburg. The project has a useful and normative validity period of 3 years (the company’s strategy can then be changed).

At the first stage, it is expected to purchase equipment (shelving, counter lighting, trade equipment, etc.) for $20,000, installation and commissioning of this equipment will amount to $3,000, and another $900 must be invested in a year. The company's total revenue at the end of the first year of the project is expected to be $120,000, of which the project itself should bring in $40,000. At the end of the first year, it is planned to pay dividends to shareholders in the amount of $6,000. Operating cash flows expected at the end of the year, expressed in prices of the initial year investments can be estimated from table 3 below (the liquidation value of the equipment is not taken into account).

Table 3. Expected operating cash flows of the project

The company makes initial investments using 40% borrowed capital at 14%, the loan must be repaid in 3 years (the method of repaying borrowed capital is annuity). The company previously incurred market research costs of $5,000.

We will generate net cash flow for the project. To do this, we will first figure out which payments we will include in the calculation and which ones we will not.

The costs of purchasing equipment, its installation and commissioning are included in the NPV. These are investment cash flows. In this case, initial costs must be reduced by the share of financing from external sources in the amount of 40%.

Initial costs will be: (20,000+3,000) *0.6 = $13,800

Project revenue, variable costs and fixed costs are also included in the NPV. These are operating cash flows. Depreciation must be separated from fixed costs and excluded from the NPV. Depreciation is a non-cash transaction.

But depreciation must be taken into account when calculating projected income taxes, which should be included in operating cash flows.

The receipt and repayment of a loan should not be taken into account in net cash flow, since this is an inflow and outflow of capital, and interest on the use of a loan should be. These will relate to financial cash flow.

The costs of marketing research, like all other previously incurred costs (sunk costs), should not be taken into account in the NPV for the project. Criterion - although these flows are related to the expected flows for the project, they cannot be monetized.

Dividends payable and other general business cash flows (such as loans, bond issues, acquisitions of financial assets) are not taken into account in the NPV, as this contradicts the “relevance” rule.

In the last year of the project, you should include the terminal value of fixed assets, because you will have the opportunity to sell fixed assets on the free market if they are no longer needed.

The terminal value of fixed assets is calculated using the formula:

First - ∑Am = 20,000 + 900 – (7,400 + 8,500 + 3,000) = $2,000

The final NPV for the investment project is formed in Table 4.

Table 4. Final NPV for the project

|

Amount, USD |

|||||

|

Investment flows |

Fixed assets + installation |

||||

|

Operational flows |

|||||

|

Variable costs |

|||||

|

Fixed costs minus depreciation |

|||||

|

Financial flows |

Loan interest |

||||

|

(13 800) |

In conclusion, we note that managing net cash flow is the second most important task for a financier after managing profitability. Understand the mechanisms for forming the NPV in your company and get an effective tool for influencing the money supply in circulation, and at the same time you will find the answer to such an important question from the manager, “Where is the money?”

I suggest watching a short video. Unfortunately, the quality of the shooting leaves much to be desired. But as a result of viewing, you will gain invaluable financial knowledge. And if you also apply them into your life, and also teach this to your child, then you will certainly become rich yourself and raise a RICH child! ;)

So, Robert Kiyosaki will reveal some of the main secrets of rich people right now.

To make it easier for you and your child to understand the information you have just received, we will consider everything in order in a simpler and more accessible form. ;)

Attention! HUGE REQUEST!

Why? It's simple! :) A child will not be able to read on his own until he remembers all the letters. The same goes for this post. It will be difficult for a child to understand the material in this article if he has not mastered the previous knowledge.

Secrets of rich people from Robert Kiyosaki.

Secret 1. The importance of financial literacy.

What is financial literacy?

Imagine that we found 100 people. And each of them was given 10 thousand rubles.

What will poor people do if they don’t know the basics of financial literacy? They will simply SPEND ALL THE MONEY on immediate desires. They will buy themselves trinkets: a new phone, new toys, spend it on entertainment...

What will rich people who know the ABCs of financial literacy do? By the end of the month they will at least DOUBLE THE INITIAL AMOUNT! :)

Did you catch the difference? :)

What are assets and liabilities?

Financial literacy begins with these concepts.

The main problem most people have is that they confuse assets with liabilities. What's the difference?

A financial asset is anything that BRINGS you money. And financial liability is everything that TAKES them away.

In other words. If you remain unemployed: assets will FEED you, and liabilities will EAT you.

Let's remember the previous example.

Poor people SPENT EVERYTHING to fulfill momentary desires (trinkets). This means that they invested their money in LIABILITIES.

The rich GOT extra money. :) This means that they invested the same amount of money in ASSETS.

Secret 2. Rich people don't work for money.

What is the difference between the poor and the middle class? It’s practically non-existent, because they SPEND their money in almost the same way.

Poor people have the only source of income - hired work. They receive income in the form of a monthly salary. They receive it and immediately spend it all on food, clothing, and accommodation. As they say, they live from paycheck to paycheck.

The cash flow of poor people looks like this: they receive income and immediately turn the entire amount into expenses.

The middle class also receives income from wage work. But their level of income in the form of monthly salary is higher than that of the poor. Therefore, they spend one part of the amount on living expenses, and the second part on buying an apartment, a car and other expensive trinkets.

What mistake does the middle class make?

Let's imagine what will happen to a representative of the middle class if he loses his hired job? The person will no longer receive a salary. That is, you will be left without income. But he will still have to spend on living expenses. And besides, you also have to maintain your expensive trinkets. Utility bills, taxes, gasoline, etc. As a result, the person decides to borrow money until he finds a new job.

What does this mean? The fact that a representative of the middle class used the second part of his monthly salary to buy LIABILITIES. And being left without work, I felt from my own experience HOW my liabilities EAT HIM UP!

By buying liabilities, he killed his golden goose, not even allowing the little chick to be born. That’s why the hen didn’t bring him any golden eggs!

The cash flow of the middle class looks like this: receive income - buy liabilities - turn into expenses.

The poor and middle class concentrate on earning active income. They trade their time for money. If you didn't show up to work, you didn't get paid.

The rich focus on creating sources of PASSIVE income. No matter what a rich person is doing at the moment, money is constantly dripping into his pocket. And this suggests that the cash flow of rich people begins with ASSETS that bring them monthly income.

It is in ASSETS that the main secret of the rich lies! Assets are the golden goose that lays the golden eggs. The rich buy all expensive trinkets in exchange for golden eggs. That's why the rich live in mansions and drive Porsches, while the middle class live in ordinary houses and drive Toyotas. ;)

The cash flow of rich people looks like this: they invest money in assets and receive income.

Everyone makes their own choice. Be poor? Or be rich?

People aren't just born rich! Those born in poverty and poverty also BECOME rich!

To BECOME rich, you need to be able to ACT as accomplished rich people do.

Every person who goes to work and receives a monthly salary has HIS CHOICE!

If a person spends money on momentary desires and trinkets (a new phone, a new toy, a trip to the entertainment center), then he CHOOSE POVERTY!

If a person seeks to increase his salary and buys expensive trinkets (a house, a car), then he CHOOSES A MIDDLE CLASS LIFE!

If a person, receiving income, buys assets, then he CHOOSES TO BE RICH!

Your choice depends ONLY ON YOU!

Secret 3. The rich work for themselves.

- Do you know what kind of business I'm in? — Ray Kroc, the founder of McDonalds, asked the students.

- What a question? Of course we know! You sell hamburgers.

- No! My business is not hamburgers! My business is real estate!

Ray Kroc meant that sales is his PROFESSION. He mainly sold hamburgers and received income from this activity.

But his BUSINESS was to create assets - he bought real estate.

Give your child the task of asking people what kind of business they are in. The answers will vary. I am a doctor. I am a lawyer. I am a businessman. But they will all be wrong! Because none of this is business! This is a PROFESSION.

PROFESSION means that you work FOR money. And BUSINESS means that your money works FOR YOU.

The main financial problem of most people is the fact that they DO NOT HAVE THEIR OWN BUSINESS!

That's all for now! ;)

If you have any questions, be sure to ask them in the comments. And I will try to help you find the answers to them! ;)

Today's article will be a continuation of the series that I opened with the article "". Today I will talk about the fundamental principle of personal finance management, which is either ignored or not taken seriously by most novice investors, and is sometimes called heresy by conservatives. As you may have guessed, today we will talk about the cornerstone of the teachings of Robert Kiyosaki, about two words that are worth thousands - about cash flow.

In simple words, this is the amount that remains in your pocket every month after you... For example, your monthly income is 100,000 rubles, and your monthly expenses - 80,000. Then your cash flow will be 20,000 rubles per month. So far it’s obvious and elementary, isn’t it? At first, it becomes incomprehensible how something so simple can be so powerful, but at the same time escape the attention of most novice investors.

The fact is that usually beginners ignore cash flow. Even if an investor uses the right formula for wealth, that is, acquires assets and gets rid of liabilities, his financial situation may remain the same or even worsen over time if he does not pay attention to cash flow. To understand what I'm talking about, let's look at an example.

Investor Vasya buys an apartment in a new building at the excavation stage

Let's say Vasya works as a programmer and receives a salary approximately three times higher than his less fortunate friends, who "got it" work as sales consultants or telephone operators somewhere in the technical support of a large telecom. Vasya is thrifty, he receives 150,000 rubles and spends 100,000 rubles, which means he cash flow is 50,000 rubles per month. Vasya loves to read books by Robert Kiyosaki and dream of financial independence... And against the backdrop of these dreams, working as a programmer becomes more and more boring for him every day... Annoying colleagues, stupid initial and eternal work on program code, which no one else in the company except him will not understand or appreciate it. Despite the large salary, work turns into a routine, and the dream of financial independence does not go away.

At some point Vasya decides: “that’s it, I’ve had enough” and a prescription using the money set aside (let it be 500,000 rubles) is going to buy Active! The search for relevant information on queries begins « « or « « . In the end, Vasya finds a new building, work on which has just begun, and the price for a one-room apartment there is only 2,000,000 rubles! "Holy shit" - that’s all Vasya can say... after all, the apartments are exactly the same size, in exactly the same houses in the neighborhood (but completed) cost from 4,000,000 rubles and above.

After spending several sleepless nights in the process of calculating hypothetical profits, Vasya comes to the conclusion that by buying this apartment now and selling it after construction is completed, in 2 years, he will be able to sell it for 2,000,000 rubles more. “This is some money!” - Vasily triumphs, a whole year’s salary! And so he runs headlong to the bank, gives his 500,000 rubles as a down payment, and receives a mortgage loan for 1,500,000 rubles. He is especially proud that the loan was issued for only 5 years in order to avoid overpaying. Vasya calculated in advance how the loan term affected the amount of overpayment and chose the most profitable option for himself.

And now, the deal is completed! Vasily has the share participation agreement in his hands. He writes down the purchased apartment in the Assets column, and a mortgage loan with a monthly payment of 40,000 rubles in the Liabilities column. This deal reduces Vasily's cash flow from 50,000 rubles to 10,000 rubles per month, and Vasya is still quite sure that he made a good deal! The next day, Vasily returns to work, makes himself coffee, sits down at the computer and, according to tradition, opens the morning HabraHabr to read.

Now attention, question! What has changed in Vasily’s financial situation? Has he become richer or poorer? Is he closer to financial independence?

Answer: nothing has changed, except that Vasily lost all his savings and significantly increased his monthly expenses.

What did Vasily do wrong?

At this point you will have to start bending your fingers.

Mistake 1. He forgot about the final goal!

Vasya dreamed of financial independence. Every night he dreamed that tomorrow he would wake up and he would not have to go to work, because he was already provided with everything he needed, but every morning he woke up...

How can you afford to quit your job? Make your passive income exceed your expenses!

What is passive income? This is a type of income that you receive automatically without working. It is created by certain types of Assets. For example, passive income will come from a rental apartment.

Let's imagine for a second that Vasily has 10 apartments, which he rents out for 20,000 rubles. This will mean that Vasily receives 200,000 monthly passive income and 150,000 income from working as a programmer. If expenses remain at the level of 100,000 rubles, then Vasily’s cash flow will be 250,000 rubles per month.

What will happen if in such a situation Vasily decides to leave work? It's OK. Cash flow will decrease and will be only 100,000 rubles per month, but this is quite enough for a comfortable life. Besides, waking up at lunchtime and lying in bed for half the day, binge-watching TV shows, when it’s Tuesday outside is priceless.

Mistake 2: He invested for capital gains, not cash flow!

What is the difference? I often hear phrases like “I bought this apartment for 2,000,000, and now it costs 3,000,000, this is a profitable investment” or “I bought these shares for 10 rubles apiece, and then sold them for 50, it was a profitable investment.” When an investor invests money in an Asset and expects the asset's price to rise, it is investing for capital gains. The catch here is that the price of an asset can go up as well as down. Even real estate can begin to lose value if the market situation is unfavorable. What can we say about the stock market... even the S&P and Dow Jones indices, which are considered the bastion of reliability, have experienced several fatal falls in their lifetime. From this we can draw a simple conclusion: investing for capital gains is very risky.

Advanced investors use both routes. They invest their funds for both capital growth and cash flow creation, while the ultimate goal is always cash flow.

Let's assume that you have an apartment that you bought for 1,000,000 and are renting out for 10,000. What happens if the price of the apartment rises to 2,000,000? It will be great and it will still earn you 10,000. What if the price then drops to 1,500,000? It will be less great, but she will still bring in 10,000. You do not lose the opportunity to sell the apartment at any time and with the proceeds buy a larger asset that will bring not 10,000, but 20,000. This is how cash flow works.

Mistake 3: He Didn't Use Leverage to Its Fullest

The down payment for the apartment that Vasily made was 500,000 rubles, which was 25% of the value of the asset. Moreover, to obtain a mortgage, it was enough for the bank to pay only 10% of the cost of the apartment or 200,000 rubles. Then 300,000 rubles could remain in Vasily’s hands, and he could dispose of them at his own discretion. For example, he could either simply start sleeping more soundly by placing them under the mattress.

This is weird. When I'm faced with a choice - have 300,000 or not have 300,000, I always choose to have. :)

Mistake 4. He chose the mortgage loan parameters suboptimally

Let's remember what Vasily was guided by when deciding on the loan term? He looked at the total amount of overpayment and tried to minimize it. His motivation is clear: he wanted to pay as little as possible for the loan in the long term. But this approach does not stand up to criticism upon closer examination. Vasily agreed with the bank to pay 40,000 rubles a month, although he could have reduced the monthly payment to 25,000 if he had been credited for 20 years rather than 5. In cash flow he would win 15,000 rubles a month!

Now the question! Would you like, starting from now, to just start receive 15,000 rubles every month? I do. An additional 15,000 per month over 5 years will turn into 900,000 rubles. And this is provided that we simply put all the money in a huge sock and occasionally allow ourselves to admire it. Imagine that we will not just store them, but use them to purchase assets that generate passive income? The benefit is obvious, isn't it?

How to develop your inner investor? Play Cash Flow

To fully understand the role of cash flow in personal finance management, I highly recommend that you play the educational game created by Robert Kiyosaki. The game is called “Cash Flow”. At this point I give the floor to Robert, he will tell you about his game!

If you want to play quickly, I can suggest an online version of the game “Cash Flow” from Russian developers. It is similar to the original, but is very much less atmospheric, so play at your own risk. :)

If you are going to get serious about improving your financial IQ, you need to buy the board version of the Cash Flow game. I’ll warn you right away: the game is not cheap, I myself doubted it for a long time before purchasing it. But then I remembered the rule: “ never skimp on education“, I bought it, and did not regret it, since the money invested paid off with interest. After the first game, I discovered a lot of new things for myself, although before that I had read Kiyosaki’s books and sincerely believed that I understood them, and I was wrong. But the most important thing is that with the help of this game I managed to interest many of my friends in the works and philosophy of Robert Kiyosaki. Having like-minded friends among me was the best gift I have ever received! Now I always feel supported and it’s much easier for me to move forward! Thanks to my friends and especially my wife, Taisiya! So be sure to play this game with your friends and family, you won’t regret it!

Good luck and more cash flow! :)

Hello everyone, Alexander Berezhnov is here.

Friends, each of my articles is my own experience gained in battle, as well as the experience of my friends, mentors and like-minded people who have gone through a lot and achieved success.

Today there are several versions of this game: Cash Flow 101, 202, 303 and 404.

All of them are designed to teach you how to competently handle personal finances, investing skills and building your own business.

How it all began

Eight years ago, a friend of mine gave me the book “Rich Dad Poor Dad” by Robert Kiyosaki to read. He said that I would definitely like it! I started studying it, and time flew by in a flash.

The book is amazing, read in one sitting. After reading it, my whole life changed! I realized that I wanted to become an entrepreneur, and subsequently, having achieved great success after a couple of decades, teach other people to do this.

While I was reading Robert Kiyosaki's book Rich Dad Poor Dad, I learned that he created the legendary real life financial simulation game CashFlow. Now it is played by millions of people all over the world; championships and trainings are held in different cities.

Rich Dad Poor Dad tells the author's life story of how he became a dollar millionaire, investor, and world-renowned financial coach under the guidance of a mentor.

The book also talks about the high moral principles of real entrepreneurs and charity.

Funny story about how I bought the game "Cash Flow"

Some time after reading this book, I decided that I would start my entrepreneurial journey with charity. I didn't hesitate and donated 10,000 rubles children's department of the Stavropol City Psychiatric Hospital.

But so that my help would definitely reach the children, I went to a good book and stationery store and bought children’s games, magnetic boards, albums, pencils, paints and other goods for the school year for the children.

By a happy coincidence, it turned out that it was in this store that the only game “Cash Flow” was sold in the city at that time. And I bought it for myself along with the “children’s” products. This purchase changed a lot in my life, strengthening my entrepreneurial spirit and allowing me to gain new acquaintances and experience!

Game description

The essence of the game– become financially independent by properly managing the SMALL personal finances that you receive in the game in the form of a salary.

Friends, everyone knows that any business must start with a goal or dream. At the beginning of the game, each participant chooses his dream. Thus, the author shows the importance of this step in the life of every person. The player who completes it the fastest wins.

There is another way to win - to significantly increase your cash flow. No wonder the game has a corresponding name.

How can you achieve your dream while working a regular job and receiving a salary?

To do this, the game has two stages:

- "Rat race" - here most people spend their entire lives until retirement, spinning like a “squirrel in a wheel”

- "Fast Lane" - wealthy people earn big money here and make their dreams come true!

During the game you will make deals, bargain and make a variety of decisions, training your financial intelligence. Here you will find ups and downs, big profits and ruins, disappointments and victories.

You will experience all these interesting moments during the game.

Friends, be sure to play Cash Flow and I assure you that you will look at your finances differently.

The game will be of interest to everyone - from a simple office worker to the owner of his own large company.

During the game you will learn:

- How to manage personal finances correctly?

- What financial instruments to invest in (real estate, stock market, bank, own business, precious metals, etc.) and how to do it Right?

- What is the difference between “linear income” and “passive”?

- What is the Cash Flow Quadrant?

- How to behave correctly if you are fired from your job?

- What are “assets” and “liabilities”?

- How to create or buy a business correctly?

During the game, just like in life, you may have children, you may be fired from your job, you may get rich or, on the contrary, go broke.

This is not just a game - it’s a whole training that will help you organize and increase your own finances.

What is the Cash Flow Quadrant?

- Wage-earners

- Self-employed workers(entrepreneurs)

- Businessmen

- Investors

- Wage-earners- these are people who perform certain functions while working for a salary. They are interested in the stability of their position and certain guarantees from the employer and the state.

- Self-employed workers(entrepreneurs) are those who have opened their own business and work for themselves, but do not have a system that provides them with income. That is, if such a person stops working, then, as in the case of an employee, his income will also tend to zero.

- Businessmen– people who have created a system that brings them income regardless of their daily labor costs. They are employers and often their business turnover is measured in very large numbers compared to hired and self-employed workers (entrepreneurs).

- Investors– receive income from investing available funds in businesses and property. Investors strive to get the highest possible return on their investments and try to strike the right balance between risks and returns on investments.

The quadrant itself is conventionally divided into left and right sides. On the left side are employees and entrepreneurs, and on the right side are businessmen and investors. Moreover, people on the right side of the quadrant are much more free and financially wealthy.

By regularly playing Cash Flow, you will understand more and more how exactly become such a person: free, rich And successful.

Reviews of the game "Cash Flow"

My colleagues and like-minded people have already played 106 games over 5 years. In particular, with my friend and co-author of the HeatherBober blog Vitaly, we played more than 30 games. At the end of each game, I asked people to provide written feedback about the game by filling out a special form with questions. Over the years I have accumulated a whole stack of such reviews.

See for yourself:

Here's what my friends say about the game:

Evgeniy Marchenko | Now I understand how to make a million dollars!Cool game, enlightening. You begin to look at life and your finances from a different perspective. The training gives real results. Now I understand how to make a million dollars! Playing “Cash Flow” for the 3rd time now, I never cease to be amazed at all the “tricks” of the game. It's especially interesting to watch people. Today I saw how a person behaves when he has free money. Most often, he begins to repay the loans and continues to remain in the “rat race”. I'm looking forward to the next game. |

Alexey Zorkin | I managed not only to have a good and useful time, but also to make very good acquaintances...I thank the presenters for their help in the strategy, for the useful information and the warm atmosphere. The game has a practical orientation. I highly recommend everyone to attend this training. Here you will learn how to properly invest your personal savings. I will be glad to meet and play with you again! Thanks a lot! Thus, I was able not only to have a good and useful time, but also to make very good acquaintances. We are still friends with these people today and cooperate in a variety of areas. |

And here are photos from our games:

I highly recommend playing Cash Flow to everyone, regardless of age or occupation. I am sure that you will spend your time usefully and at the same time gain very good practical knowledge and interesting experience!

All this will help you further improve your financial situation. Play the game more often with friends and business partners. I especially recommend this game to those who have problems planning their finances.

Where to buy the game "Cash Flow"

In large cities, the game can be found in large bookstores or specialized board game stores.

But there this game in the board version will cost 30-50% more, so it is much more profitable to order it via the Internet.

There are many different dubious online stores, but I prefer to order only from the most reliable and trusted ones, for example, from the online store ozon.ru (free delivery within Russia)

And remember, as he himself says

“The more often you play Cash Flow, the richer you become!”

Robert Kiyosaki

This is true because you begin to think more effectively, and as a result, your actions change, allowing you to achieve the best results!

Here's a live video of Robert Kiyosaki talking about his acting: (3:55)

Dear readers, what do you think about this game? What other business games do you know? Share your opinions and reviews in the comments!