How to add a division to 1s 8.3. Creation of a separate division

Legal entities have the right to create separate divisions for various purposes. The legislation regulates in detail the conditions and procedure for their creation. Separate divisions simultaneously have two main characteristics:

- The address of a separate division differs from the address of the organization indicated in the Unified State Register of Legal Entities;

- At the location of the separate unit, at least one stationary workplace is equipped for a period of more than a month.

In the 1C:Accounting 3.0 program, created on the 1C:Enterprise 8.3 platform, registration of a separate division is carried out in the menu “Directories - Enterprises - Divisions”.

Fig.1

You need to create a new division in 1C: check the “Separate division” box, fill in all the details, indicate the head division. The division will have its own checkpoint, and the TIN will be common for all divisions and the parent company.

Fig.2

After filling out, the document must be recorded, and then it will be reflected in accounting.

Fig.3

In the 1C program, you can create, configure and maintain records of several organizations and departments at the same time. At the same time, it is possible to separately calculate wages with the submission of tax reports to different Federal Tax Service Inspectors. Let's look at an example of how to keep records for separate divisions in terms of wages.

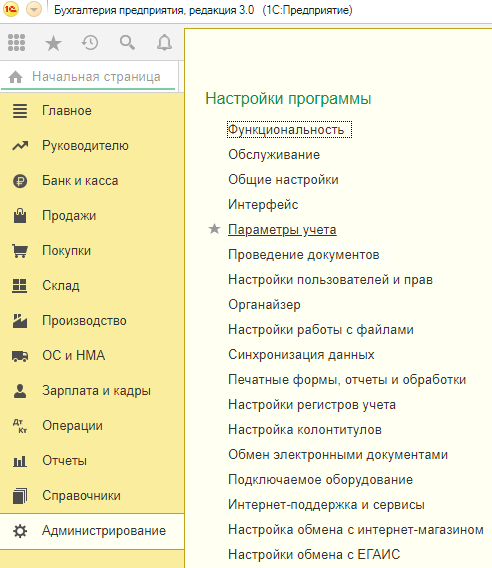

In the main menu, select “Administration – Program settings – Accounting parameters”.

Fig.4

In the accounting parameters, select “Salary settings”.

Fig.5

In the “Payroll calculation” section, check the “Payroll calculation by separate departments” checkbox.

Fig.6

In the department card you can enter the details of the tax office to which the reports will be submitted.

Fig.7

Payroll

First we need to hire employees for our division. To do this, go from the main menu to “Salaries and personnel – Personnel records – Hiring”.

Fig.8

Through “Create” we go to the employment document. We fill in the following information:

- The organization is our organization;

- Division – a separate subdivision;

- Position – position of an employee of a separate unit;

- Employee – an employee of a separate unit;

- Reception date – fill in the required date;

- Probation period – fill in if one is provided;

- Type of employment – in our case it is internal part-time work.

Fig.9

Now let’s calculate the salary of the employee of the main and separate division. Salaries in 1C 8.3 are calculated in the section “Salaries and Personnel - Salaries - All Accruals”.

Fig.10

Using the “Create” button, we calculate wages for employees of the main department. For example, let's take data for one employee. We will fill out and post the “Payroll” document.

Fig.12

Generation of 2-NDFL certificates

So, we have calculated wages for two employees of the main and separate departments. Next, we will generate 2-NDFL certificates for these employees. To do this, from the main menu go to “Salaries and personnel – personal income tax – 2-NDFL for transfer to the Federal Tax Service”.

Fig.13

We create a certificate for an employee of the main department. The 1C 8.3 program offers the opportunity to select a tax office according to OKTMO and KPP. We select the one we need and fill in the remaining data. The employee data should be filled in automatically. The help displays the following information:

- The tax rate is in our case 13%;

- Income – accrued salary to an employee;

- Taxable income - if there were no deductions, then the amounts are the same;

- Tax – the amount of accrued personal income tax;

- Withheld – personal income tax is withheld at the time of salary payment, our salary has only been accrued, so in our case the value in this cell is “0”;

- Listed – this field will be filled in after the tax is paid to the budget, so for now it is also “0”.

Fig.15

Next, fill out a certificate for an employee of a separate unit. We generate the certificate in a similar way, changing the data in the OKTMO/KPP field when paying income. Data from the Federal Tax Service at the address of the separate division. Similar to the previous certificate, the employee’s data, his income, tax rate and tax amount are filled in automatically.

Fig.16

Just like for the previous certificate, you can display a printed form in which we see the Federal Tax Service code different from the first one.

Fig.17

In this article, we looked at how to create a separate division, as well as the possibilities offered by the 1C 8.3 program for payroll, tax calculation, as well as submitting reports for employees of the main and separate divisions to different tax inspectorates. Thanks to them, maintaining a separate unit in the program will not be difficult for users.

When working in the 1C: Accounting 8 version 3.0 program, you need to make a choice at almost every step. Due to the fact that organizations and types of activities are very diverse, all options must be reflected in accounting, which accordingly leads to an increase in the functionality of the program, which is often very difficult for an accountant to navigate. To make this task easier, the program has a new function that will help you with your work.

It is known that accounting software is capable of performing many different functions, but is all of them necessary for a particular company and accountant? As practice shows, an organization does not always require the full functionality of the program. This causes additional inconvenience for the accountant, since each time he enters the program, he needs to run his eyes through unnecessary objects - menu items, buttons, icons, etc., which are not used in the organization’s accounting. Of course, these extra elements will not contribute to fast and convenient work. In addition, the configuration provides many “reminders” and services that may also be unnecessary for an accountant. This problem was resolved by introducing a new feature that allows you to disable unused program elements.

Previously (before release 3.0.35), turning on and off some functions was done in the form of setting “Accounting Parameters”. It remained there, but the path to the settings became shorter

The visibility of most functions can be adjusted by pressing one of the three buttons offered: “Custom”, “Main”, “Full”. The comments from the electronic assistant will help you make your choice.

You can find out what this or that functionality implies on the form tabs. With “Basic” all checkboxes are cleared, and with “Full” all checkboxes are checked. With "Custom functionality" you can determine which options should be disabled and which ones should be left. Please note that if you initially selected “Basic functionality” and then added some options, or vice versa, after selecting “Full functionality” you disabled some of the functions, then the program will automatically install “Custom functionality”.

If the work is performed in a new information base, then the settings will not provide restrictions within the full functionality of the program. If you need to reduce functionality in a working infobase, the program will issue a warning about which settings cannot be changed due to the fact that they were used during processing of historical data.

Cost accounting by departments and without

Program "1C: Accounting 8" ed. 3.0 has another equally useful feature, which is the ability to keep track of costs without dividing them into departments (the feature is available starting from version 3.0.35). It allows the accountant to perform a much smaller number of actions in the program, which means completing the work much faster.

The main users of the 1C:Accounting configuration also include small businesses that do not have separate divisions. Previously, the standard setting of the Chart of Accounts only provided for cost accounting by department.

This function is necessary to solve an important management task - detailing costs by departments that take part in the production of products or the provision of services. This process can be simple or complex, including several stages. Moreover, depending on what type of activity the enterprise conducts, as well as on the complexity of the product and the required resources, the stages can take place in one or several departments.

But the bulk are not large enterprises, but small and medium-sized ones that provide similar services or produce technologically simple products. In addition, when the staff of an organization includes only a few people, there can be no talk of a full-fledged unit. Therefore, in such cases, the mandatory filling of the Division field previously created additional inconvenience in the work.

Now cost accounting by department can be disabled, so the accountant does not have to waste time filling out unnecessary fields. To do this, simply uncheck the box on the Production tab in the Accounting Parameters settings and then save the selected parameter.

Now, a non-existent division (for example, Main), as well as unnecessary fields in the program, do not need to be filled out.

Since version 3.0.52in "1C: Accounting 8 CORP" edition 3.0automated calculation of income tax when deregistering separate divisions. We talk about the features of filling out a set of income tax returns for organizations during the liquidation of separate divisions and about how the calculation of income tax is reflected in “1C Accounting 8 CORP” (rev. 3.0) for cases where the tax base has increased and decreased.

The procedure for calculating and paying tax upon liquidation of a separate division

If an organization has decided to terminate the activities of its separate division, and the head has signed an order for its liquidation, then the tax authorities must be notified of the decision within 3 working days (clause 3.1, clause 2, article 23, clause 6, art. 6.1 Tax Code of the Russian Federation).

The application is submitted in form No. S-09-3-2 (approved by order of the Federal Tax Service of Russia dated 06/09/2011 No. ММВ-7-6/362@) to the Federal Tax Service inspectorate with which the organization is registered at the location of the liquidated unit. In "1C: Accounting 8 CORP" (rev. 3.0) this form is available as part of 1C-Reporting(chapter Notifications - Separate subdivisions - Closure of segregated subdivisions).

Within 10 days from the date of filing such an application (but not earlier than the end of the on-site tax audit, if one is carried out), the inspection is obliged to deregister the organization (clause 5 of Article 84 of the Tax Code of the Russian Federation). From this moment on, the separate division is considered liquidated.

If a responsible separate division is liquidated (through which income tax is paid and which submits an income tax return for a group of separate divisions located on the territory of one constituent entity of the Russian Federation), then a new responsible division must be selected and within 10 days after the end reporting period, notify the tax authorities about this (clause 2 of Article 288 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of Russia dated December 30, 2008 No. ШС-6-3/986). The notification forms are given in the Appendices to the said letter.

The specifics of calculating and paying income tax by a taxpayer who has separate divisions are defined in Article 288 of the Tax Code of the Russian Federation. Let us recall that for the reporting (tax) period, the tax base for income tax is determined by the cumulative total for the organization as a whole, and then distributed between the parent organization and separate divisions in proportion to the share of each division, which is calculated on the basis of 2 indicators:

- the share of the residual value of depreciable property of this division in the residual value of depreciable property throughout the organization;

- the share of the average number of employees of a given division in the average number of employees of the entire organization, or the share of expenses for remuneration of employees of a given division in the total amount of expenses for remuneration of employees of the entire organization (in “1C: Accounting 8 KORP” only this option is supported).

At the same time, the rules for calculating and paying income tax upon liquidation of separate divisions are not explained in Article 288 of the Tax Code of the Russian Federation.

At the same time, the rules for calculating and paying income tax upon liquidation of separate divisions are not explained in Article 288 of the Tax Code of the Russian Federation.

Let us turn to the procedure for filling out a tax return for corporate income tax (approved by order of the Federal Tax Service of Russia dated October 19, 2016 No. ММВ-7-3/572@, hereinafter referred to as the Procedure). According to clauses 10.2 and 10.11 of the Procedure, when closing separate divisions during the tax period:

- in subsequent reporting and current tax periods after the closure, the tax base determined for the organization as a whole is reduced by the tax base attributable to closed separate divisions;

- the share of the tax base attributable to a closed separate division and its size are determined for the reporting period preceding the quarter in which the division was closed.

Thus, the last reporting period when the share of the tax base (profit share) for the liquidated division is determined is (letter of the Federal Tax Service of Russia dated October 1, 2009 No. 3-2-10/23@, Federal Tax Service of Russia for Moscow dated July 12, 2010 No. 16 -15/073317):

- for quarterly reporting taxpayers - the quarter preceding the quarter in which the separate division was liquidated;

- for monthly reporting taxpayers - the period from the beginning of the year to the last day of the month preceding the month of liquidation of the separate division.

When closing a separate division, updated declarations, as well as declarations for subsequent (after closure) reporting periods and the current tax period for the specified separate division, are submitted to the tax authority at the location of the parent organization (clause 2.7 of the Procedure).

Income tax calculationin “1C Accounting 8 CORP” (rev. 3.0)

Starting from version 3.0.52, 1C:Accounting 8 CORP (rev. 3.0) supports automatic calculation of income tax when deregistering separate divisions due to:

- moving - changing the address at which the activity is carried out;

- termination of the division's activities.

To reflect these events in the program, you should use the commands available from the directory element form Divisions(from the card of a separate division or branch) - see fig. 1:

Rice. 1. Separate unit card

When calculating income tax and filling out the declaration, the requirements of clauses 2.7, 10.2 and 10.11 of the Procedure are taken into account.

The tax base has increased

Let's consider how the 1C: Accounting 8 CORP program, edition 3.0, automatically calculates profit shares and generates tax returns if one of the separate divisions is closed during the year.

Example 1

|

The organization Comfort-Service LLC applies OSNO, the provisions of PBU 18/02, and at the end of the reporting period pays only quarterly advance payments. The organization Comfort-Service LLC is registered in Moscow, and has two separate divisions, which are located in St. Petersburg and in Anapa (Krasnodar Territory) and are registered with the Federal Tax Service at their location. Transfer of advance payments (tax) to the budget of a constituent entity of the Russian Federation is carried out by the parent organization (Moscow). At the end of the first half of 2017, the tax base for income tax for the organization as a whole amounted to RUB 381,370. Over 9 months, the tax base increased and amounted to RUB 1,262,645. The income tax rates for the budgets of the constituent entities of the Russian Federation do not differ and amount to 17%. In August 2017, a separate division located in St. Petersburg was deregistered (liquidated). Data for the first half of 2017 are shown in Table 1 (indicators in lines 1 and 2 are rounded). Table 1 Tax base and calculated income tax for budgets and constituent entities of the Russian Federation for the first half of 2017

|

Since the separate division in St. Petersburg was liquidated in August 2017, the last reporting period for it will be the first half of 2017. Figure 2 shows a fragment of Appendix No. 5 to Sheet 02 of the income tax declaration (hereinafter referred to as the Declaration) for the first half of 2017, compiled for a separate division in St. Petersburg.

Rice. 2. Appendix No. 5 to Sheet 02 of the Declaration for a separate division in St. Petersburg for the six months

In July 2017, during a routine operation Income tax calculation included in processing Closing the month, in relation to each separate (including the head) unit, standard actions are performed:

- the share of profit (share of the tax base) is automatically calculated based on labor costs and the residual value of depreciable property;

- based on the calculated share of profit, the tax base is determined;

- Based on the tax base and the tax rate established for a specific constituent entity of the Russian Federation, the amount of tax is calculated;

- Postings are generated in the context of budgets and inspections of the Federal Tax Service of Russia.

In August 2017, a separate division located in St. Petersburg is closed.

In August 2017, a separate division located in St. Petersburg is closed.

Therefore, when performing a routine operation Income tax calculation for August, in addition to standard actions with existing units, special actions are carried out in relation to a closed separate unit:

- the share of the tax base (profit share) is fixed in the amount calculated for the reporting period preceding the quarter in which the separate division was closed (clause 10.11 of the Procedure), that is, for the first half of 2017 (33.0256%). The specified share remains unchanged (“frozen”) until the end of the tax period, that is, until the end of 2017;

- the tax accrued for July is adjusted and fixed in the amount calculated for the first half of 2017 (RUB 21,412). The amount of accrued tax does not change until the end of the year, provided that the tax base for the organization as a whole does not decrease.

Starting from August 2017, in the calculation certificate Distribution of profits among the budgets of the constituent entities of the Russian Federation the fixed share of the profit of a closed division is indicated separately - in the group Activities have been discontinued(Fig. 3).

Rice. 3. Help-calculation of profit distribution according to budgets for September 2017

According to the calculation certificate, the share of the tax base (profit share) for operating divisions for 9 months of 2017 was:

- at the head office in Moscow - 93.2203%;

- for a separate division in Anapa - 6.7797%.

We will create it in the service 1C-Reporting a set of tax returns for 9 months of 2017.

, in the Title Page, by default, the details of the head unit (Moscow) are set, namely:

- in field - indicate the code of the tax authority in which the

head office registered (7718); - in field - the code is indicated: 214 ( At the location of the Russian organization that is not the largest taxpayer).

The main sheets and indicators of the Declaration, including Appendix No. 5 to Sheet 02, are filled in automatically according to tax accounting data (button Fill).

The income tax declaration, which is submitted at the location of the head division, includes Appendix No. 5 to Sheet 02 in the amount of 3 pages, corresponding to the number of registrations with the Federal Tax Service from the beginning of the year (for the head and 2 separate divisions, including closed ).

Let us first consider how the program fills out Appendix No. 5 for a closed, separate division in St. Petersburg (Fig. 4).

Rice. 4. Appendix No. 5 to Sheet 02 of the Declaration for 9 months for a closed separate division

In field Calculation completed (code) the value will be indicated: 3 - for a separate division closed during the current tax period. The following line indicators are filled in automatically:

- Tax base for the entire organization(line 030) - 1,262,645 rubles;

- including without taking into account separate divisions closed during the current tax period(line 031) - 1,136,695 rub. This indicator corresponds to the difference between lines 030 for 9 months of 2017 and 050 for the first half of 2017 of Appendix No. 5 to Sheet 02 for a closed separate division (RUB 1,262,645 - RUB 125,950);

- Tax base share (%)(line 040) - 33.0256% (the fixed share of the tax base for a closed separate division corresponds to line 040 of Appendix No. 5 to Sheet 02 for the first half of 2017);

- Tax base based on share(line 050) - 125,950 rub. The difference between the indicators on lines 030 and 031 must correspond to the indicator on line 050 for a closed, separate division (clause 10.2 of the Procedure);

- Budget tax rate subject of the Russian Federation (%) (line 060) - 17%;

- Tax amount(line 070) - 21,412 rub. This indicator corresponds to the indicator of line 070 of Appendix No. 5 to Sheet 02 for the first half of 2017.

Line 080 ( Tax accrued to the budget of a constituent entity of the Russian Federation) is filled in manually by the user - RUB 21,412. (line 070 of Appendix No. 5 to Sheet 02 for the first half of 2017). Under the conditions of Example 1, the amount of tax to be paid additionally (line indicator 100) is zero.

Appendix No. 5 to Sheet 02 Declarations drawn up for the head division and for a separate division in Anapa are filled out based on the tax base for the organization as a whole, excluding closed separate divisions and the share of the tax base calculated for 9 months. Figure 5 shows a fragment of Appendix No. 5 to Sheet 02 of the Declaration drawn up for the head unit. In field Calculation completed (code) the value will be indicated 1 - for an organization without separate divisions included in it. Field imposing the obligation to pay tax on a separate division must be filled in manually (specify the value 1 - assigned).

Rice. 5. Appendix No. 5 to Sheet 02 of the Declaration drawn up within 9 months for the parent unit

The indicators of lines 030-070 are filled in automatically as follows:

|

Data |

|

|

RUB 1,262,645 |

|

|

RUB 1,136,695 (tax base for 9 months of 2017 minus the indicator of line 050 of Appendix No. 5 to Sheet 02 for the first half of 2017 for a closed separate division: RUB 1,262,645 - RUB 125,950) |

|

|

RUB 1,059,631 (line 031 indicator multiplied by line 040 data) |

|

|

RUB 180,137 (line 050 indicator multiplied by line 060). The sum of lines 070 of Appendix No. 5 for the parent organization and for each separate division is transferred to line 200 of Sheet 02 (clause 10.4 of the Procedure) |

Line 080 is filled in manually by the user and must correspond to the indicator in line 070 of Appendix No. 5 to Sheet 02 for the first half of 2017 for the parent division. Line 100 ( Amount of tax to be paid) is calculated automatically as the difference between lines 070 and 080.

Appendix No. 5 to Sheet 02 for a separate subdivision in Anapa is filled out in the same way.

Subsection 1.1 of Section 1 of the Declaration for the head unit will be automatically filled in according to the declaration data.

Line 010 of Subsection 1.1 of Section 1 indicates the OKTMO code of the municipality in whose territory the head office is located.

Now it is necessary to fill out declarations for separate divisions: active (Anapa) and closed (St. Petersburg).

When filling out a tax return, which is submitted at the location of a separate division in the city of Anapa, on the Title Page the user must indicate the appropriate code of the tax authority, selecting it from the list of registrations, and the code of the place of submission of the declaration: 220 ( At the location of a separate division of the Russian organization).

By button Fill the program will automatically generate a set of Declaration sheets for a separate subdivision in Anapa.

Appendix No. 5 to Sheet 02 is filled out similarly to the corresponding page of Appendix No. 5 to Sheet 02 Declarations, which is presented at the location of the head unit.

Filling out an income tax return for a closed division has its own peculiarities.

When creating a new report version Income tax return On the title page, the user must perform the following sequence of actions:

- in field Submitted to the tax authority (code)- indicate the tax authority code of the closed separate division by selecting it from the list of registrations (7801);

- in field at the location of registration (code)- specify code: 223 ( At the location (registration) of the Russian organization when submitting a declaration for a closed separate division);

- confirm your actions (button Yes) to the program warning ( Attention! Before entering the filling mode for separate divisions, all sections (sheets) of the report will be cleared. Continue the operation?).

As a result, the details on the Title Page (Sheet 01) of the Declaration are dynamically refilled and take on the following values in accordance with clause 2.7 of the Procedure:

- in field Submitted to the tax authority (code)- indicate the code of the tax authority of the head division (7718), where it is now necessary to submit a declaration for a closed separate division;

- in field checkpoint- the checkpoint of a closed separate subdivision is indicated (780132001).

By button Fill the program will automatically generate a set of Declaration sheets for a closed, separate division.

Appendix No. 5 to Sheet 02 is filled out similarly to the corresponding page of Appendix No. 5 to Sheet 02 of the Declaration, which is submitted at the location of the head unit.

On line 010 of subsection 1.1 of Section 1, the 1C: Accounting 8 CORP program, edition 3.0, will indicate the OKTMO code of the municipality on the territory of which the closed, separate division was located (clause 4.1.4 of the Procedure).

The tax base has decreased

Example 2

If the tax base for the organization as a whole decreases, compared to the previous reporting period and the reporting period after which the separate division was closed, the previously calculated tax is subject to reduction:

- for the organization as a whole;

- for separate divisions, including closed ones.

To do this, it is necessary to recalculate the tax base based on the fixed share of the profit of the liquidated division (clause 10.11 of the Procedure, letter of the Ministry of Finance of Russia dated August 10, 2006 No. 03-03-04/1/624, Federal Tax Service of Russia dated October 1, 2009 No. 3-2-10 /23@, Federal Tax Service of Russia for Moscow dated February 18, 2010 No. 16-15/017656).

To do this, it is necessary to recalculate the tax base based on the fixed share of the profit of the liquidated division (clause 10.11 of the Procedure, letter of the Ministry of Finance of Russia dated August 10, 2006 No. 03-03-04/1/624, Federal Tax Service of Russia dated October 1, 2009 No. 3-2-10 /23@, Federal Tax Service of Russia for Moscow dated February 18, 2010 No. 16-15/017656).

Thus, in accordance with clause 10.11 of the Procedure, when closing a separate division, the program checks whether the profit for the entire organization has decreased compared to:

- with the previous reporting period;

- with the reporting period after which the separate division is closed.

If both conditions are met, then to calculate the tax base for a closed separate division, the fixed share of the tax base (indicated in the declaration for the last reporting period for this division) is taken and multiplied by the total profit for the organization. Otherwise, the tax base for a closed division is assumed to be equal to the tax base indicated for this division in the declaration for the last reporting period.

Let’s say that the tax base decreased in September 2017 (for example, expenses increased sharply). When performing a routine operation Income tax calculation for September, the following actions are carried out in relation to a closed separate unit:

- Based on the fixed share of profit, a new tax base is determined, reduced compared to the first half of 2017 - RUB 33,026. (RUB 100,000 x 33.0256%);

- The tax calculated for the first half of 2017 is adjusted downward and amounts to RUB 5,614. (RUB 33,026 x 17%).

The tax base for the organization as a whole, excluding separate divisions closed during the current tax period (line 031), is also reduced and now amounts to RUB 66,974. (RUB 100,000 - RUB 33,026). In relation to each operating separate (including the head) unit, the following actions are performed:

- The share of profit (share of the tax base) is automatically calculated;

- based on the calculated share of profit, the tax base is determined (for the head office in Moscow - 62,433 rubles, and for a separate division in Anapa - 4,541 rubles);

- based on the tax base, the amount of tax is calculated (for the head office in Moscow - 10,614 rubles, and for a separate division in Anapa - 772 rubles);

- Reversing entries are generated for accrued tax in the context of budgets and inspections of the Federal Tax Service of Russia.

Figure 6 shows a fragment of Appendix No. 5 to Sheet 02 of the Declaration for 9 months of 2017, compiled for a separate division in St. Petersburg with a decrease in the tax base. Since the tax base has decreased, there is an overpayment of tax, including for a closed separate division. The issue of offset (refund) of tax overpaid at the location of the liquidated separate division must be considered by the tax authority registered with the parent organization (letter of the Ministry of Finance of Russia dated March 17, 2006 No. 03-03-04/1/258). Offsetting the amount of an overpaid advance payment for a closed separate division against the payment of income tax at the location of the parent organization located in another constituent entity of the Russian Federation is legal (letter of the Ministry of Finance of Russia dated February 24, 2009 No. 03-03-06/1/82, Federal Tax Service of Russia in Moscow dated May 30, 2011 No. 16-15/052700).

Rice. 6. Appendix No. 5 to Sheet 02 of the Declaration for a closed separate division when the tax base is reduced

14.09.2018

How to enable the ability to maintain records for Separate divisions in the standard configuration "1C: Enterprise Accounting KOPR"

General information

The standard configuration of 1C: Enterprise Accounting, version 8 of KORP, allows you to organize end-to-end accounting in the context of organizational units, both allocated and not allocated to a separate balance sheet.

The CORP version allows you to set up accounting for separate divisions for the receipt and transfer of fixed assets, finished products, materials, cash, as well as the transfer of employees between the parent organization and separate divisions.

The KORP version of the "1C: Enterprise Accounting" configuration allows you to keep track of income, expenses, and profits for each separate division. When preparing an income tax return, distribution shares according to the Federal Tax Service are calculated, which greatly facilitates the work of an accountant.

For each separate division, you can indicate the addresses, telephone numbers, and names of the responsible persons of the division. This data is displayed in printed forms of all documents issued by a separate division. Separate numbering of documents by separate divisions is supported.

Buy 1C: Accounting CORP for 33,600 rubles. right now!

Also, the KORP version of the "1C: Enterprise Accounting" configuration allows you to organize the accounting of payments for state defense orders in accordance with the requirements of Federal Law No. 275-FZ dated December 29, 2012 (taking into account amendments to Federal Law No. 159-FZ dated June 29, 2015).

How to enable accounting by separate divisions

To enable the ability to create Separate divisions in the standard configuration of "1C: Enterprise Accounting KORP" version 3.0, you need to check the "Accounting for several organizations" and "Separate divisions" flags in the functionality settings window on the "Organization" tab (see figure).

We agree with the warning “Enabling functionality may take a long time.”

After this, the “Organizations” item will appear in the “Main” section.

A directory of organizations and separate divisions will open.

Click the "Create" button.

A window will open in which you can select which organization we are adding: individual entrepreneur, new legal entity or separate division.

In the next window, you can specify the details of the Separate Division: Name, checkpoint, Prefix (if separate continuous numbering of documents in the separate division is required) and Digital code for invoices, OGRN, registration date, address, telephone, bank details, full names of the responsible persons of the separate division divisions (which must be indicated in documents issued on behalf of the OP), data from the Federal Tax Service, Pension Fund of the Russian Federation, Social Insurance Fund and statistics codes.

The TIN of a separate division and the taxation system are the same as those of the Parent organization and cannot be changed.

After specifying all the details of the Separate Unit, click on “Record” or “Record and Close”.

The separate division will appear in the "Organizations" directory. Now you can select a Separate Division in any document.

To increase the convenience and speed of work, each user can be assigned a Separate Department by default, which will be immediately automatically inserted into documents when they are created, and if necessary, you can set up an access restriction system so that users of a separate department can write out and see only documents of their separate department and not saw the documents of the Parent Organization and/or other divisions.

Please note that full support for working with Separate divisions is implemented only in the standard configuration "1C: Enterprise Accounting" rev. 3.0 version of CORP. There are no plans to include these functionalities in the Basic and Professional versions!

Cost of "1C: Accounting 8 KORP"

You can purchase 1C: Accounting KORP from our company, even if you are in another region of the Russian Federation. The price includes remote installation of electronic delivery and sending boxed versions by courier throughout the Russian Federation.

There are several options for delivering the software product "1C: Accounting 8 CORP":

| Name | Price | Description |

|---|---|---|

| 1C:Accounting 8 CORP | Boxed delivery of "1C: Accounting" version of KORP with a software protection system with a license for 1 workplace | |

| 1C: Accounting 8 CORP. Electronic delivery | Electronic delivery of "1C: Accounting" version of KORP with a software security system with a license for 1 workplace | |

| 1C:Accounting 8 KORP (USB) | Boxed delivery of "1C: Accounting" version of CORP with a USB hardware dongle for 1 workstation |

Advantages of electronic delivery of "1C: Accounting 8 KORP"

- Purchasing an electronic delivery allows the user to receive installation distributions and activation codes for 1C software products as quickly as possible.

- The electronic delivery is generated at the time of purchase, so the user receives the current version of the program at the time of purchase.

- Documentation and accompanying materials are supplied in a convenient electronic format, which allows you to immediately see the contents of the book and quickly move to the desired chapter.

- The software product is registered in your personal account on the official 1C technical support portal immediately at the time of purchase and the user gets access to all updates to the technology platform and standard configuration immediately, without the need for additional registration.

Discount when upgrading from 1C:Accounting 8 PROF and previous versions

You can get a discount when upgrading 1C: Accounting from the PROF version to KORP in our company, even if you purchased 1C: Accounting PROF elsewhere and are in another region of the Russian Federation. The main condition is that the 1C: Accounting PROF set to be handed over must be licensed and officially purchased.

If you have previously used 1C: Accounting 8 PROF, then this gives you the right to purchase 1C: Accounting 8 CORP at a significant discount. When upgrading, you will only need to pay the difference in price between PROF and KOPR versions of 1C:Accounting 8 according to the current price list + 150 rubles. For example, if you previously purchased 1C: Accounting 8 PROF (at the time of writing, the price list price is 13,000 rubles), then when upgrading to 1C: Accounting 8 CORP, the cost of the additional payment will be 33,600 - 13,000 + 150 = 20,750 rubles.

When upgrading, the price of the purchased 1C: Accounting 8 CORP set includes 3 months of a preferential subscription to information technology support for ITS. Also, when upgrading, it is possible to extend the preferential ITS subscription period from 3 to 12 months at a special price of 19,776 rubles, which makes it possible to make the transition to the CORP version even more profitable. For example, a regular ITS PROF subscription for 1C:Accounting PROF for 12 months at the price list costs 35,992 rubles, and the cost of an upgrade from PROF to CORP version is 20,750 rubles. + extension of the preferential ITS subscription when purchasing the program from 3 to 12 months. - 19776 rub. The total cost of the upgrade + ITS for 12 months will cost 40,529 rubles, i.e. the amount of additional payment for the transition from PROF to CORP version will be 4934 rubles! The rest of the amount will go towards payment for the ITS subscription, which you would already have to pay for the maintenance of 1C: Accounting PROF.

Online version of "1C:Accounting CORP" in the cloud service 1C:Fresh

Cost from 495 rub./month. per user*

Today, “1C: Accounting KORP” can not only be purchased and installed on your computer, but also used remotely via the Internet in cloud service mode. In this case, the 1C: Accounting KORP database is located on secure servers in the 1C data center, and users can work in the program remotely via the Internet using a regular web browser (Chrome, IE, Edge, Mozilla, Safari) or 1C thin client (provided free of charge).

Access to the online version of "1C: Accounting KORP" is provided on the principles of SaaS (software as a service - program as a service).

Our company is an official partner of the 1C company with the status "1C: Network Competence Center", which gives us the right to connect users to the cloud service "1C: Fresh" on the same conditions for the entire Russian Federation and at the price established by the 1C company.

The 1C website has a page for auto-registration https://online.1cfresh.com, which allows our users to independently register in the cloud service.Upon initial registration, our users are provided with free access for the first 30 days of connection, then the cost of access will cost from 495 rubles* per month per user, depending on the number of users, number and size of information databases.

Cost of access to the online version of 1C:Accounting 8 KORP in the cloud service 1C:Fresh

Tariff plan 1 month 3 months 6 months 12 months 1C: Accounting CORP

Access for up to 10 simultaneous users

594.00 rub. per month

for 1 user

535.40 rub. per month

for 1 user

516.60 rub. per month

for 1 user

494.40 rub. per month

for 1 userAdditional workplace (over 10 users)

The indicated price includes access to up to 10 simultaneous users (sessions) to two 1C: Accounting CORP information databases up to 8GB in size + connection to electronic reporting for 1 legal entity + connection to the 1C: Counterparty service for auto-filling the details of counterparties by TIN and checking them against the database Federal Tax Service + the ability to use other configurations available in the service (1C: Enterprise Accounting PROF/Basic, 1C: Salaries and Personnel Management, 1C: Managing Our Company) without limiting the number and size of information databases.

* Cost 495 rub./month. per user is calculated when connecting 10 users and paying for 12 months.

If everything worked out as it should, then like the article on social networks and share the link on your favorite forums))).Online Company, 2018

Separate division in 1C, How to set up a separate division in 1C: Accounting KORP, 1C 8.3 separate division, 1C Accounting separate division, How to create a separate division in 1C 8.3 accounting, How to create a separate division in 1C Accounting KORP rev.3.0, Accounting for separate divisions in 1C: Accounting KORP, changing the address of a separate division in 1C Accounting, Opening a separate division in 1C Accounting KORP, Where to indicate tax data for a separate division of 1C Accounting KORP, How to add a separate division in 1C Accounting KORP, 1C Accounting Personal Income Tax separate division, How to create a separate division in 1C separate division, 1C 8 separate division, changing the head of a separate division in 1C Accounting, how to open a separate division of LLC in 1C Accounting, paying taxes by separate divisions, how to register a separate division in 1C Accounting, How to create a separate division in 1C Accounting CORP, Separate division in 1C Accounting KORP, A separate division in a standard configuration Enterprise Accounting 1s 8.3, Accounting for separate divisions in 1s 8.3, 1s corp separate divisions, How to create a separate division in 1C Accounting 8.3 version KORP, How to maintain a separate division in 1C Accounting KORP, Separate division 1s 8.3 in the directory of organizations, Create a separate division in 1C 8.3, FSS separate division in 1C Accounting, separate division profit calculation in 1C Accounting, Dedicated balance sheet of a separate division in 1C Accounting KORP, How to create separate divisions in 1C, separate division allocated to a separate balance sheet in 1C Accounting KORP, Separate accounting of a separate division in 1C Accounting, How to enter a separate division in 1C, Order to create a separate division in 1C Accounting, 1C 8.2 separate division, cash book of a separate division, parent organization and separate division in 1C Accounting KORP, personal income tax on separate divisions in 1C Accounting, How to set up accounting for separate divisions in 1C Accounting CORP 8.3, How to add a separate division in 1C, How to add a separate division in 1C Accounting CORP, Separate divisions in 1C 8 3, How to create a separate division in 1C Accounting in another region, Property tax of separate divisions in 1C Accounting, Documents for a separate division in 1C Accounting, Separate division step-by-step instructions, taxation of a separate division in 1C Accounting, Create a separate division in 1C Accounting 8. 3 versions of KORP, How to add a checkpoint of a separate division in 1C Accounting KORP, 1C KPP of a separate division, How to create a balance sheet for a separate division in 1C Accounting KORP, 6-NDFL separate division in 1C Accounting KORP, 1C Accounting KORP NDFL separate division, accountant of a separate division, Calculation of contributions to funds for a separate division in 1C Accounting, How to create a separate division in another city in 1C Accounting, How to maintain a separate division in 1C, How to create a separate division in 1C 8.3, Tax accounting for a separate division in 1C Accounting, cash desk of a separate division 1C , organization of activities of a separate division in 1C Accounting, Separate division of a legal entity in 1C Accounting, Separate account of a separate division in 1C: Accounting, How to enter a separate division into 1C, How to indicate information about a separate division in 1C Accounting, Calculation of contributions to the Social Insurance Fund for a separate division in 1C Accounting, Separate accounting of the profit of a separate division in 1C Accounting, Balance sheet of a separate division in 1C Accounting, 1C Accounting how to create a separate division, Income tax of a separate division in 1C Accounting, How to add a separate division in 1C 8.3, Location of a separate division in documents 1C Accounting, 1C 8.3 corp separate division, Accounting of a separate division in 1C Accounting, Reporting of a separate division in 1C Accounting, How to make a separate division in 1C, checkpoint of a separate division invoice 1C Accounting, Calculation of contributions to the Pension Fund of the Russian Federation for a separate division in 1C Accounting , Declaration of a separate division in 1C Accounting, Head of a separate division in 1C Accounting, Create a separate division in another city in 1C Accounting, invoices of separate divisions 1C, Work of separate divisions in 1C Accounting, How to fill out a separate division in 1C, legal address of a separate division in 1C Accounting, Where to indicate the current account of a separate division in 1C Accounting, 1C income tax separate division, Calculation of contributions for a separate division in 1C Accounting, Representative office (separate division) in 1C Accounting, create a separate division in 1C 8.3 accounting, Director of a separate division in 1C Accounting, accounting for a separate division + in 1C 8. 3 accounting, Separate division reports in 1C Accounting, How to create a separate division of your organization in 1C, 1C accounting accounting for separate divisions, separate division of a company in 1C Accounting, implementation for a separate division in 1C, Calculation of taxes for a separate division in 1C Accounting, accounting for separate divisions, 2-NDFL of a separate division in 1C Accounting, Contributions for a separate division in 1C Accounting, 1C Accounting 3.0 separate division, 1C 8.3 separate division, Tax accounting of a separate division in 1C Accounting, Profit for separate divisions in 1C, insurance contributions of a separate division in 1C Accounting, 1C cash book of a separate division, Income tax for separate divisions in 1C, How to enter a separate division in 1C 8.3, a separate division located outside the location of the parent organization in 1C Accounting, Invoice of a separate division in 1C Accounting, separate division in 1C 8.3 corporate accounting, Numbering of invoices of a separate division in 1C Accounting, 1C accounting 3.0 separate divisions, Profit declaration of a separate division in 1C, Separate accounting of the property of a separate division in 1C Accounting, setting up a separate division in 1C 8.3, Head and separate division in 1C Accounting, 1C reporting of separate divisions, Calculation for a separate division in 1C Accounting, 1C 8.3 checkpoint of a separate division, organization of accounting for a separate division in 1C Accounting, Cash desk of a separate division in 1C 8.3, Income tax declaration of a separate division in 1C Accounting, Separate division of a branch organizations in 1C Accounting, VAT of a separate division in 1C Accounting, branches and other separate divisions in 1C Accounting, How to create a branch in another city in 1C Accounting, accounting policy of a separate division in 1C Accounting, Registration with the tax authorities of a separate division, details of a separate division in 1C Accounting, how to reflect the formation of a separate division in 1C Accounting, a separate division taxes and reporting in 1C Accounting, a separate division of a limited liability company in 1C Accounting, Accounting for income and expenses, as well as actual profit for each separate division in 1C Accounting KORP

Tags: How to add a separate division in 1C Accounting KORP, 1C Accounting Personal Income Tax separate division, How to create a separate division in 1C, 1C 8 separate division, changing the head of a separate division in 1C Accounting

If you decide to keep payroll records in the 1C 8.3 Accounting program, then starting from version 3.0.44.115 it supports division into separate divisions. Please note that this functionality is only available if the organization has up to sixty employees. The basic version of 1C does not support such accounting.

In this article we will look at how to configure separate divisions in 1C 8.3 using an example. We will also show the possibility of submitting tax reports separately to different Federal Tax Service Inspectors.

Setting up the program and adding a new unit

First of all, you need to make some preliminary settings. They are located in the “Administration” - “Accounting Settings” section.

In the window that opens, select the “Salary Settings” item.

If you are just starting to keep track of payroll in this program, you need to indicate this in the “General Settings” section. Otherwise, you will not have access to the relevant documents.

In the "Payroll" section, check the box as shown in the image below. It is he who is responsible for the capabilities of payroll accounting for separate divisions.

Now we can begin to create and configure separate units.

Let’s assume that the Kopleksny trading house has a separate division in the city of Klin. To reflect this in the program, we need to set a flag on the item of the same name in the card of this unit.

In the “Tax Inspectorate” section, we can create another Federal Tax Service Inspectorate, to which reports from this division will be submitted. Let's indicate that its number will be 5099. In the future, we will look at how this will look using the example of a personal income tax certificate.

Personal income tax reporting for separate divisions

Before forming any amount on employee wages, it must be accrued. This can be done in the “Salaries and Personnel” - “All Accruals” section.

First, we created a payroll document for August 2017 for the Kompleksny trading house, indicating a separate division in the city of Klin.

Only one employee was included in the tabular section - Vasily Stepanovich Petrov. He worked the entire month, for which he was paid a salary of 60,000 rubles.

Let’s assume that this employee also works in the head division of the Kompleksny trading house, which is not separate. In August 2017, he also worked the entire month and received a salary of 80,000 rubles.

It turns out that employee Vasily Stepanovich Petrov worked simultaneously in both the head office and a separate unit. Let's consider how these data will be reflected in the 2-NDFL certificate, which can also be found in the “Salaries and Personnel” section.

In the form of generating a certificate, we need to select which Federal Tax Service it is intended for. In the “OKTMO/KPP” field we will indicate the data of the inspection that we indicated earlier in the separate unit card. We will generate a report for 2017, in which the above accrual was made.

As you can see in the figure below, this certificate included only one line with information about the employee - V.S. Petrov. At the same time, please note that the amount is only 60,000 rubles. The fact is that even though two accruals were made for him, separate reporting is submitted to another tax office.

The printed form of this certificate will also reflect the Federal Tax Service code – 5099.

When selecting other OKTMO/KPP for which there were accruals, our employee will also appear in the tabular section, but with an amount of 80,000 rubles. This data was downloaded from the head office payroll.

Thus, the 1C: Accounting program allows us to keep records and submit tax reports for separate divisions to different tax inspectorates. This mechanism fully complies with the requirements of current legislation.